Ugandan Anti-Corruption Sign (credit: futureatlas.com, CC BY 2.0)

There’s been some concern about government insiders demonstrating great skill at choosing investments, at the presumed expense of other investors (not just individuals, but pension funds and other entities on which we depend). At least they’re required to, ex post, report their trades, including those of their spouses. But there must be a better solution.

A lot could be accomplished by reducing the role of government, and government-backed monopolies such as the “Federal” Reserve, in our economy. This would reduce the leverage of gov’t insiders. But every government operation has a lobby behind it, so this will be a challenge to accomplish. And even a legitimate limited government is going to have an impact on the economy.

So I propose that government insiders be required to post all their trades in advance, let’s say at least an hour before executing them. Put them on an easily-accessible public website (insiders.gov might be a good URL) so folks can front-run them. It would create a whole new subindustry of forecasting market moves based on what the insiders are doing.

Of course all kinds of new hustles might develop to get around this.

Posting a trade and then not executing it

Having offshore trusts which they can claim not to control

Telling their friends a day ahead of time what they plan to do

But it would at least be progress. And it might discourage some of the wealthy from getting so directly involved in government.

Disused Chicago bread factory to become data center. Image credit: Emily CC BY-NC 2.0

In a new article (archived copy, also included in this pdf) for the Chicago Council on Global Affairs, Cook County Assessor Fritz Kaegi asks “In a digital economy, how can cities create a more equitable property tax system?” Of course he does not try to define “equitable,” but one infers from the article that it means “funded more by those benefiting from the digitalization of the economy, and less by those who actually perform useful work.” A desirable result, to be sure, but how does he propose to accomplish it? He also seems to assume that government-funded schools are a good thing, or at least that parents shouldn’t be held individually responsible for arranging their own children’s education.

He proposes to get more revenue from the big infotech companies, specifying Apple, Microsoft, Alphabet/Google, Amazon, and Facebook, but by implication the numerous other organizations who have prospered by taking advantage of the internet (as well as their lobbying capabilities to stifle competitors). He doesn’t think that local or state government is equipped to collect much of this revenue. Further, he assumes that a real estate tax to fund “education” can only be implemented at the school district level, and couldn’t be countywide, regionwide, statewide, or in any respect subnational. He concludes that the U S government needs to send large quantities of money to America’s cities, particularly including Chicago and the rest of Cook County.

“The federal government … is best situated to tax incomes generated by activity like digital commerce, virtual meetings, and footloose service providers [and]…will need to build fiscal mechanisms for a digital world that separates economic activity from physical space. ” (Presumably these wealthy and influential companies won’t use their influence to deflect the tax burden to others. )

OK, so Cook County local governments don’t get revenue from this digital economy? What about the 11 (soon to be 12) data centers in Elk Grove Village (archived copy), paying real estate taxes and utility taxes, as well as taxes imposed on persons working to construct and operate them. This report (archived copy) counts 52 data centers regionwide as of February 2021. Both reports note that several kinds of tax favors are provided, without indicating that they’re necessary since the digital economy requires facilities in appropriate locations.

And Amazon and other on-line retailers don’t generate taxes? Those of us who’ve bought something on line in the past couple years have noticed that the e-commerce giants collect and remit state and local sales taxes, typically in excess of 10% here. Last year the BGA counted (archived copy) 36 warehouses in the Chicago area built for Amazon since 2015 (and noted “at least $741 million in taxpayer-funded incentives”). This of course doesn’t count warehouses used by non-Amazon sellers such as Walmart and Target. Again, it’s likely that most or all of these facilities would have been built without subsidies, since warehouses have to be located appropriately with respect to markets, labor supply, transportation, etc.

Kaegi is legitimately concerned about the fragmentation of Cook County’s tax base, noting that “The lower the value of real estate in a community, the higher the effective rate to provide a comparable level of school services. This results in

great disparities.” But that problem isn’t inherent in the real estate tax; it’s inherent in the fragmentary structure of finance, funded largely by local real estate tax. A statewide real estate tax, such as Illinois had until it was replaced by a sales tax in 1933, could reduce or eliminate the disparities. A number of states retain statewide real estate taxes, but the problem of disparities can also be addressed by a tax-base sharing arrangement, as has operated for half a century in Minnesota.

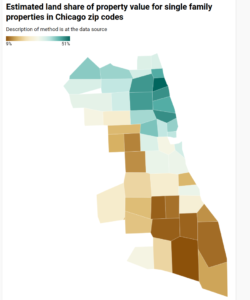

“[W]e must continue to push for local-school funding that is not rooted in local land values,” writes Kaegi. Actually, if an effective disparity-reduction arrangement is in place, the opposite might be true. I have previously posted a table and map illustrating that, if taxes were based on land value rather than land+improvement value, the burden on homeowners in communities of low income and color would be lessened. And of course if the burden of sales taxes could be replaced by a tax on land value, the benefit to moderate-income households would be enhanced.

So we have an Assessor, running for re-election, who doesn’t believe the taxes he helps calculate are a good way to fund local services. I had hoped for better (but didn’t really expect it), as the quality of assessment seems to have improved during his tenure. He does have one announced primary opponent.

UPDATE Aug 29 2021: If anyone familiar with Chicago doubts that removing improvements from the tax base will ease the burden on low-income homeowners, this map will be instructive. The original, mapless post from Aug 25 follows.

We sometimes are told that a land value tax (LVT) would punish the poor person who has a small rundown house on a high-value lot, while benefiting the person next door who has a large fancy house on an identical lot. And that’s not wrong, it’s just atypical. In practice, we believe, poor people mostly live in neighborhoods where housing is cheap and land is cheaper, thus they would tend to benefit from a shift to LVT.

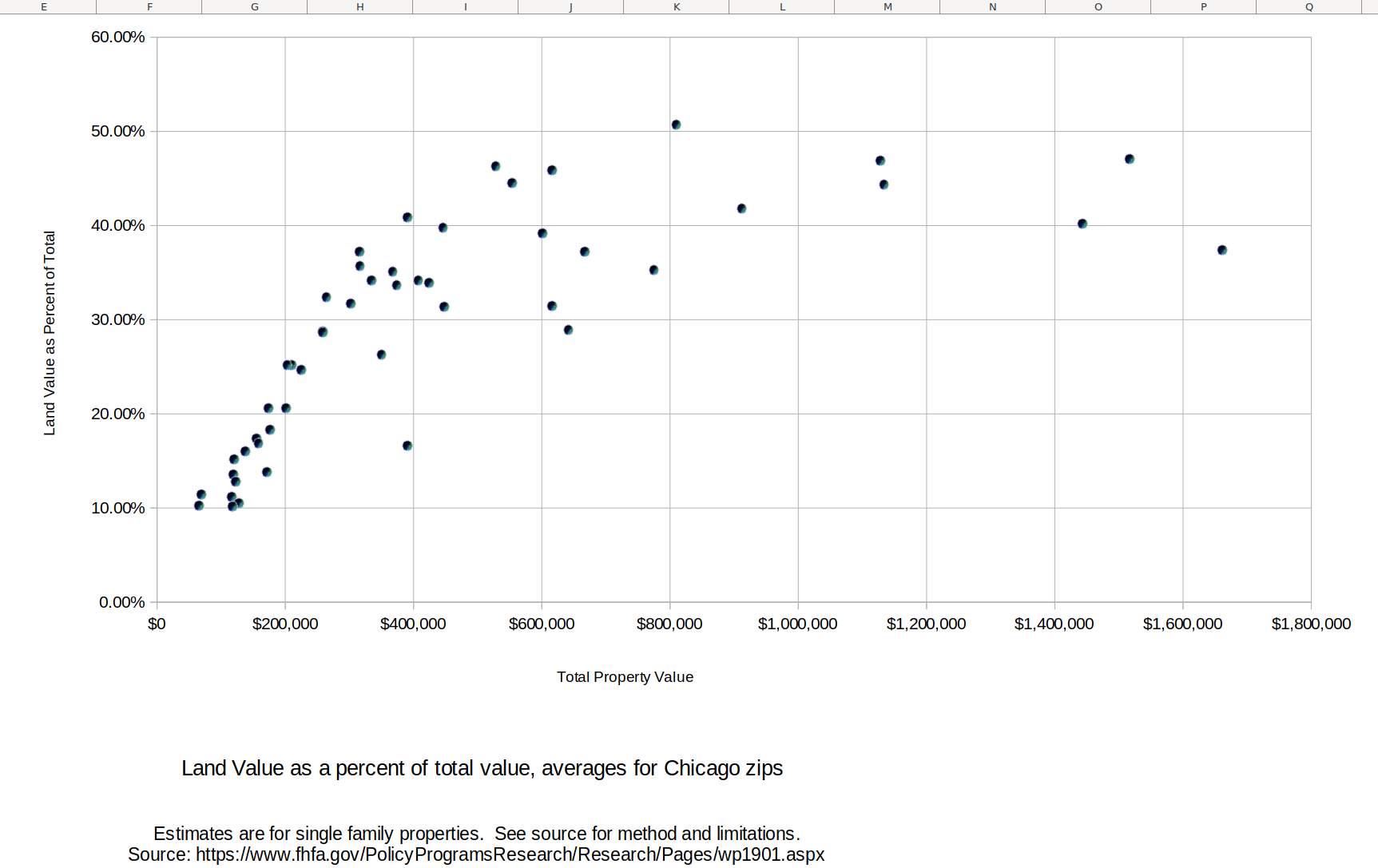

As the quality of Cook County assessments has been improving, we expect to be able to show this by analysis of that data. In the meantime, we have some estimates of land and improvement value from William Larson and colleagues at the Federal Housing Finance Agency. Using appraisals produced for mortgage underwriting, they estimate land and improvement values for homes in most zip codes (and census tracts) nationwide. Their source data includes only single family properties which were appraised for mortgage purposes. They consider only parcels where the improvement is less than 15 years old, and exclude vacant land as well as land where the appraised value is very close to the assessed value (in case appraisers might have relied on low-quality or obsolete assessments). Also excluded are zip codes with an insufficient number of single family home transactions.

The chart below shows, for Chicago zip codes, the ratio of land value to total value (vertical axis) and total value of the property (horizontal axis. What stands out is that the ratio tends to be lower where the properties are cheaper. That is, a revenue-neutral shift of property taxation to land values only, ignoring value of improvements, would tend to reduce the taxes on low-value zip codes, while increasing it in higher-value areas.

The table below shows the data for each zip code, sorted from high proportion of value in land to low. Clearly the more affluent areas have lower proportion of improvement value, and the areas with low income population have a higher proportion of improvement value.

Estimated land value proportion and related data for single family properties in Chicago zip codes

Also of interest, even tho the low-value areas have a high ratio of improvement to land value, this isn’t because of large houses on small lots. The floor area ratio is generally lower in the areas with lower land value proportion.

Overall, the above data is consistent with Georgists’ assertion that low-income residents usually benefit from a switch to LVT. I might be taking a further look at this dataset.

Thanks to Center Square via Wirepoints for alerting me to a (weekly?) mortality tally from the CDC. It provides weekly counts of death by underlying natural cause, for each state. For Illinois, unredacted Covid-19 deaths started with the week ending March 21, and the report covers the 22 weeks thru August 15. Counts for 2019 as well as 2020 are shown. My tally below attributes to Covid those deaths where it is an “underlying cause.”

Covid All other Total

Year 2019 N A 43,223 43,223

Year 2020 6,779 46,537 53,316

So if I am interpreting this correctly, we seem to have had 46,537-43,223=3314 excess deaths, not due to Covid, but possibly due to the plandemic lockdown measures. Given that most Covid victims had co-morbities, which might for some have proved fatal without Covid, this figure must be an understatement. Further, if some excess deaths are due to people not getting routine screening or treatment during the lockdown, those might not show up until some time hence.

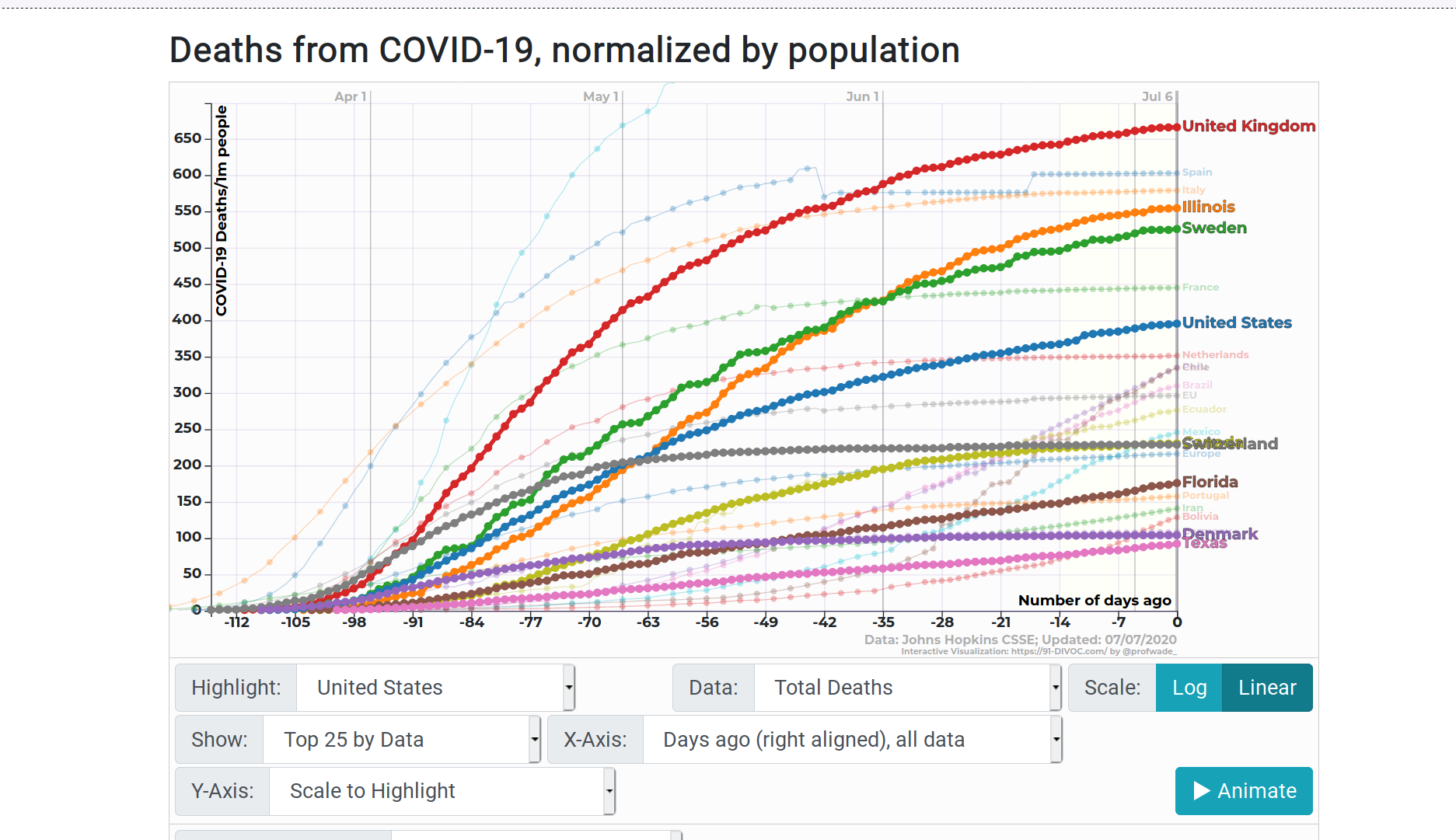

(The country you can’t see, overwritten by Switzerland, is Canada.) What I make of this is that maybe the Swedish approach, relatively unrestricted, works about as well as the Illinois approach, pretty locked down except for big demonstrations. Otoh, if the Danes are similar to Swedes, then the former nation’s lockdown might have been quite helpful in reducing deaths. To a level almost as low as Texas, tho we’ll see how that works out in the coming month or so.

Go play with the site, recently enhanced to allow comparisons between U S states and nations. It’s great fun.

I was only a bit surprised to find that Chicago’s 2020 police budget is $1,778,002,408, or $660 for each of the 2,693,976 folks that DJ Trump’s Census Bureau estimates live in Chicago. This doesn’t include $737.5 million for the police pension fund, nor $204,867,834 for the Office of Emergency Mgt and Communications, nor $135 million for “judgments and settlements against the City,” (including but not limited to police misbehavior), nor the police-related portion of the City’s capital budget, which seems to include the “joint public safety training academy” ($85 million, but just $15.75 million in the current year), and some other facilities. All told, and without doing the detailed analysis which I wish the Civic Federation would do, it seems the the City spends something like $1000/person/year for police. That doesn’t necessarily mean that police should be defunded in whole or in part; after all, reported crime has for the most part been declining, so perhaps we are getting something for our money. But it gives some idea of the dollars involved. (And it turns out that, as I was writing this, the Civic Federation produced a post covering much the same ground, with better context and detail and colorful charts, and noting that I failed to include some undetermined but substantial benefit costs among the cost of police.)

Compare police costs to Chicago Public Schools. CPS is a separate unit of government, but controlled by the Mayor and funded mainly by Chicago property tax payers. For the current year, it’s planning to spend $7.84 billion, or $2910 per Chicago resident. Enrollment continues to decline, 13% in ten years (roughly the same amount as reported crime, but that might just be a coincidence).

Summing the police and school expenses, Chicago spends $3910/person. For the hypothetical family of four, that’s over $15,000. I wonder how many two-worker households would prefer to have one stay home, help educate the children, hiring tutors as needed, and keep an eye on the neighborhood, if their income increased by that amount. Just a thought.

Update September 27: It turns out I’m not the only one suggesting that we spend too much on government schools.

It’s certainly true here, where owner-occupants (of houses or condos) pay less tax than renters occupying units of the same value, with additional discounts for old people, some military veterans, and some poor old people. Some owners also still benefit from deductability of mortgage interest and/or property tax. So why do renters put up with this discrimination?

I have always thought, and some data seems to confirm, that it’s because homeowners vote, and renters don’t. But according to this interview, the problem is similar, perhaps worse, in Australia. Voting in Australia is compulsory, which apparently means one is fined if one fails to at least show up at the polls (the fine is up to $79AU, less for their Federal elections). They also vote on Saturday, and seem to make a party of it, according to various posts such as here and here.

Of course just showing up doesn’t mean that you vote, nor that you pay much attention to candidates and issues, but the problem of low-information voters isn’t unique to Australia. Maybe there’s something about the worldview of people who rent vs. that of people who own….? Dunno.

U S jurisdictions do often provide some protections for tenants, which can disadvantage landlords, but they wouldn’t affect the status of owner occupants.

As Polly Cleveland continues her project posting Mason Gaffney’s works, we find “Chicago’s Growth Spurt, 1890-1900.” It’s not very long, and worth reading today as a contrast to our current stagnation. Most importantly, Gaffney deduces circumstantial evidence that during the era of growth, land values were significantly taxed. As he notes in conclusion, “More research into Chicago’s political history is needed.”

The whole trove contains dozens of working papers, class notes, and publications, in Gaffney’s concise and understandable style. (You’ll find it linked here as well as above; depending on your screen size and magnification you might need to scroll over to the right to see it.)

We hear that corporate tax rates, at 35% (federal), are too high and need to be reduced so U S companies can be competitive. I remain confident that the best way to fund public services is thru a tax on land value and other measures of privilege, but if any kind of corporate tax is to be retained, here are a few things to consider:

The statutory rate is 35%, but there are all kinds of credits and deductions a corporation can take, so typically the effective rate is much less. Here’s a U S Treasury report (pdf) claiming that effective corporate tax rates were 20% in 2011, the most recent year calculated. Major corporations have the ability to obtain special tax favors. (Just scan thru the tax code (big pdf) to find some of these special favors, available only to individual projects or corporations which reached specific milestones on specific combinations of dates.)

Enterprises in most countries, but not in the United States, have to pay a national value-added or sales tax. The rate and details of course varies by country, but is typically about 19% as indicated by this OECD spreadsheet. Scroll down to the second half of this article to get some more perspective from John Hussman.

Most U S states impose an additional corporate income tax, with varying rates and rules. Illinois takes 9.5%. I have no knowledge about other states nor subnational jurisdications outside the US. However, this table from Deloitte (pdf) provides some detail, including an assertion that the total national+local corporate tax rate in Germany is about 30-33%.

Some commentators complain about “double taxation” of corporate earnings, because corporate dividends are paid out of after-tax earnings. However, incorporation, with its perpetual life and limitation of liability, is a privilege, for which it’s reasonable to expect corporations to pay. I don’t suppose that taxable income is the best measure of the value of this privilege, perhaps a small percentage of total expenditures would be better, but certainly the appropriate fee is greater than zero. Furthermore, a considerable percentage of corporate stock is owned by various kinds of entities which do not pay tax, such as universities and other nonprofits, and Roth IRA’s.

_(14596109179).jpg)