We have a Libertarian Party candidate for Cook County Assessor who apparently hasn’t learned the lessons of California’s Proposition 13. So he wants to do something similar here. Too late to do anything about that, I suppose, so this post is aimed at anyone thinking about running for Assessor in 2030.

The candidate proposes to “limit property taxes to 1% of assessed value with annual inflation increases capped at 2%.” In fact, the Assessor has no power to set property taxes, and is required to assess property at a predetermined percentage of his estimate of its market value. Changing that would require action from the State Legislature, and probably also the Cook County Board.

An Assessor candidate seeking tax reform might be successful with a different proposal: Simplify assessments by excluding all buildings and other improvements, taxing only the value of the land as vacant, and gradually increase the tax rate to eliminate the need for sales tax, income tax, and other prosperity-killing taxes. Of course this would also require cooperation from the State and County, but at least it would remove the burden on production, reducing the cost of living (including housing) and encouraging entrepreneurs who hire people to do useful things.

This 2030 Assessor candidate would need to improve the assessment of land value (assuming that the prior Assessor hasn’t done so) to realistically reflect what each site is worth. Then Cook County can move toward a true libertarian tax system. The Ultimate Tax Reform.

Cannon at Morris, IL (credit: Joseph Gage, CC BY-SA 2.0)

I am not saying that anything that follows is unlawful. It should be, but very possibly it isn’t.

Bisnow informs us of another data center being built, this one at Morris in Grundy County. More information is posted by the developer. It’ll take 343 acres, and was purchased for $51.5 million. That’s over $150,000 per acre.

So what was its assessed value? I haven’t the exact parcel numbers, but parcel 02-26-200-00, 40 acres which appears to be part of the site, is currently assessed at $23,139, or $578/acre (implying a market value of $1,753/acre). Taxes appear to be $1636 for the year 2024. And the parcel was purchased in 2023 for $8,788,076.00, or $219,702/acre.

Of course this can be entirely legal under farmland assessments, in which the market value of the land for nonagricultural use has little to do with the assessment. Maybe a State in financial distress would want to think about another way to handle this.

Thanks to Dr. Robert Malone for linking to a Fox interview with Musk and members of the DOGE team. They talk about the kind of problems they’ve found, and assert that they’re working on fixing them. Worth watching despite the excessively friendly interviewer.

Lots of waste and fraud, as well as inefficiency, being found. But Musk, and some of the other DOGE people, are or work for important government contractors. Were no problems found with any of these contracts? How would such problems be handled?

Then, at the close, Musk talks about the need to end the Ukraine war. “[T]housands of people are dying every day in trenches…” Well, a lot of people are dying, and I suppose some of them are in trenches, but it’s not “thousands…every day.” There are numerous partial estimates, some behind paywalls or regwalls, but if we look at the Wikipedia article (“The number of civilian and military deaths is impossible to determine with precision”) we see numbers definitely less than “thousands every day.” Which does not mean that the war should not end, but does imply that maybe Elon is being a bit loose with some of his numbers. I wonder if the same might apply to the earlier parts of the interview.

Tribune reports (via yahoo news, alternative link) that a portfolio of 812 lots, nearly all in Chicago, will be sold as a result of bankruptcy of the owner. Apparently a couple of north suburban residents were holding them in hopes of speculative gain, but amassed fines and back taxes such that the lots are now to be auctioned off.

The Tribune interviewed some potential bidders who hoped to build housing or commercial structures on the sites.

The article does not bother to mention that Cook County taxpayers provide at least two special benefits to owners of vacant lots. First, because there is no improvement on the lot, only the land value is taxed, whereas similar lots containing buildings would pay much more. And second, it is County policy to assess vacant land at only 10% of market value, whereas commercial and industrial uses would are assessed at 25% (unless granted special favors).

If Cook County omitted all improvements from assessments, and levied taxes based on land value only, a considerable tax burden would have been shifted to speculators from homeowners and others who productively use their land. And this bankruptcy sale, getting the land back into use, would have happened much sooner (or perhaps the owners would never have tried to speculate in land).

The wildfires aren’t completely controlled at this writing (January 15), but they will be. Estimates of dollar loss are all over the place, the highest I’ve seen is $275 billion. Maybe it’ll be more; let us suppose $400 billion is the cost to replace the buildings and other wealth that has been lost. Let us further suppose that half of that will be covered by insurance from solvent companies. Finally, let us suppose that it is public policy to compensate private individuals and corporations for their losses, even tho no such compensation is provided to victims of common thieves.

So who should pay this $200 billion? Well, the US Federal government has lots of money and can issue bonds as needed to obtain more. But it’s already over $36 trillion in debt, ignoring some big obligations. Ultimately the money will come from federal taxpayers, of whom we may assume there are about 200 million (The total number of personal returns filed appears to be less, but some are joint.) That would work out to $1,000 per taxpayer, tho of course more for those who lack effective lobbyists and less for those who don’t.

But why should this be a Federal matter at all? Why can’t the people of California, or even of Los Angeles County, cover the cost? They’re certainly closer to the situation. The County Assessor tells us that the total assessed value of taxable property in the County is $2.1 trillion. But like other jurisdictions, this involves many fictions, and the actual value of any given property is typically several times the assessed value. In California this seems to be largely due to Proposition 13.

It seems that in LA County, at least for residential parcels, the land value is typically much greater than the improvement value. [edit 1/18/25: This article and link therefrom supports the assertion that “[l]and values in Los Angeles account for an extremely high share of home value.”] What this means is that, if you bought a house and lot for $1,000,000, and the house was destroyed, you actually lost less than $500,000. Combining the Countywide underassessment with the relatively high proportion of value in land, the $2.1 trillion in total assessed value probably includes actual land value greater than $2.1 trillion. And if this value were taxed at, say 1%, it would yield more than $21 billion/year that could fund recovery and rebuilding. (This 1% would be in addition to the much lower effective rate already applied.) There is no need for Federal taxpayers to bear this burden, which benefits primarily owners of very expensive real estate.

This is essentially how San Francisco recovered from its 1906 earthquake, as documented by Mason Gaffney in this article.

This seems to be another tax gimmick (is not everything about the income tax a tax gimmick?), that can be used by owners of agricultural land. It’s called a “legacy nutrient deduction,” and if I understand it correctly, when you buy farmland, your purchase includes the fertilizer resident in the soil. Over time, the quality or quantity of fertilizer degrades, so you can deduct the loss in value. It’s not exactly “land” as Henry George envisioned it*, and it does open some opportunities for clever and affluent folks. Who otherwise might be engaged in productive tasks.

I do wonder whether, if glyphosate leeches out of the soil, that might increase its value and perhaps should be taxed.

*Or maybe it is. “Your land itself is not quite so good. You have been cropping it, and by and by it will need manure.”

CTA locks down Red Line extension funding, reports the Sun-Times. Contracts have been signed, and apparently the thing will be built, despite availability of a much cheaper and sooner alternative.

Sun-Times reports the total cost of the extension to be $5.75 billion. CTA say it’s 5.5 miles long, so that works out to about $16,500 per inch. They say it’ll handle 40,000 rides/day, which, allowing for weekends and holidays and maybe a scamdemic or two, comes to about 12 million rides/year. If it lasts 50 years, that’s 600 million rides. So that’s $5.75 billion/600 million, or about $9.58/ride.

image credit: Raed Mansour CC BY 2.0

Assuming the forecasts are correct.

Service is already available in this area, from Metra Electric and CTA and Pace buses, but it might not be as fast(?) and convenient as a Red Line extension would be. But my question is, if you told everyone affected that, instead of riding an extended Red Line, you would pay them$9.58 to ride a bus or Metra train, how would they respond? Over 220 workdays/year, that’d work out to over $21,000. Enough to buy and operate a car, I suppose.

Recognize, too, that $5.75 billion is only the capital cost. It doesn’t pay the train operators, customer assistants, maintenance staff.

Continuing our exploration of land values and real estate taxes in Cook County …

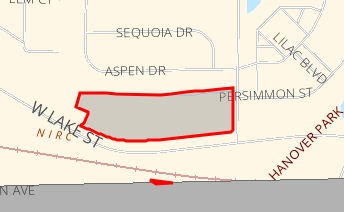

Parcel #06364020270000, at 1830 Lake St in Hanover Park. 7.36 acres, adjacent to a residential area and virtually across the street from a Metra station. Due to favors done for class 239 farmland owners, it pays less than $200/year in property tax.

The County contains 813 parcels coded as class 239 “non-equalized land under agricultural use, valued at farm pricing.” An explanation of how farms are supposedly assessed is included in this document, page 12 of which states:

The assessor notes each of the farm’s land use categories and uses the equalized assessed value for each soil productivity index to determine the assessed value. The assessor may make some subtractions for things like slope, drainage, ponding, flooding, and field shape and size before calculating the final value. • The portion on which crops are planted is assessed at the state-certified equalized assessed value certified by the Department for the corresponding soil productivity index. • Permanent pasture is assessed at one-third of what would be assigned if it was planted in crops. • Other farmland (e.g., forestland, grass waterways) is assessed at one-sixth of what would be assigned if it was planted in crops. • Wasteland has no assessed value unless it contributes to the productivity of the farm.

For Cook County, the Assessor provides specifics here.

The total assessed value of these 813 parcels is $2.25 million. To calculate their acreage it seems I would have to retrieve the records manually and individually, but the 2022 Census of Agriculture says the County contains 154 farms totaling 10,281 acres. (A farm might comprise several parcels). This implies an assessed value of $218/acre. Reviewing a small sample of parcels, it appears that the Assessor values most class 239 parcels at $2250/acre, and assesses them at 10% of that, or $225/acre.

One might compare this to the Illinois Society of Farm Managers and Rural Appraisers’ report, which includes but doesn’t break out Cook County, and indicates sales prices in Northeastern Illinois range from $5500 to $40,000 per acre.

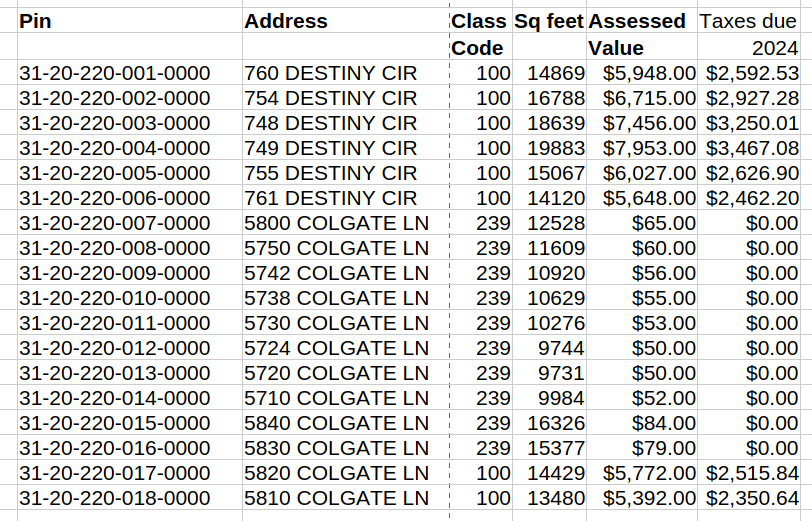

There’s no minimum parcel size for a “farm” under class 239. Thus, we have a series of 18 small vacant lots in Matteson: 31-20-218-001-0000 thru 31-20-218-018-0000. All of these appear to be empty lots, awaiting the construction of houses. Eight of them are classified as vacant land, with assessed values ranging from $5392 to $7953 (differences apparently due to differing sizes). Taxes due on these in 2024 range from $2351 to $3467 (excluding overdue taxes from the prior year, but including interest charged). But ten of these similar lots are class 239, farmland, assessed at $50 to $84. The County issues tax bills of zero for these parcels. This is claimed to be due to 35 ILCS 200/18-40, which states

If the equalized assessed value of any property is less than $150 for an

assessment year, the county clerk may declare the imposition and collection of

all tax for that year to be extended on the parcel to be unfeasible and

cancelled. No tax shall be extended or collected on the parcel for that year

and the parcel shall not be sold for delinquent taxes.

However, these parcels are assessed at $50 to $84. Applying the equalization factor of 3.0163 results in EAV greater than $150. In response to my inquiry, the Cook County Treasurer explained that, even tho equalized assessed valuation is printed on the tax bill, it isn’t used for taxation of farm properties. Here are the 18 parcels:

18 vacant lots in Matteson

I don’t know why 10 of these properties are assessed as farmland while 8 are not.

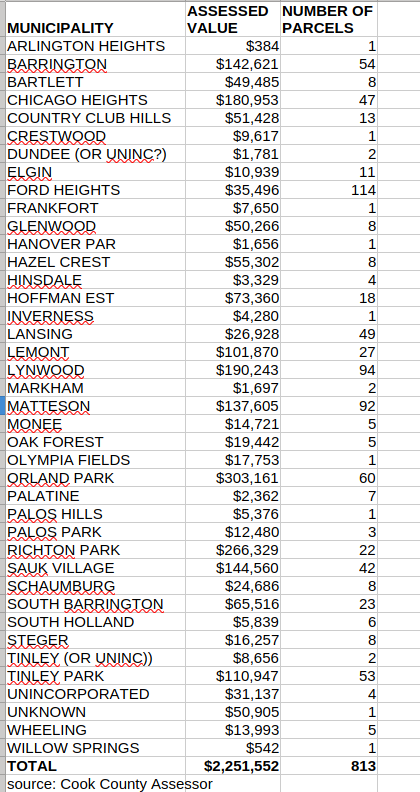

Countywide, the 813 class 239 parcels have a total assessed value of $2,251,552. While the Assessor’s records are imperfect (there being, for example, no “Dundee” municipality in Cook County), it appears that only 37 of the County’s municipalities (plus a few unincorporated areas) contain class 239 parcels. The tally is shown in the following table. Keep in mind that these are assessed value, 1/10th or less of the actual market value.

Summary of Class 239 parcels by place

While class 239 is a great bargain for owners of “farmland,” the inequity doesn’t seem, by itself, to have a major effect on the financial condition of the taxing bodies. For example, Ford Heights has the largest number of class 239 parcels, 114. Total class 239 assessed value in Ford Heights is $35,496. If this land was subject to equalization like other parcels, the equalized assessed value would be $107,067. As noted above, the Assessor seems to undervalue class 239 parcels, but even if we assume undervaluation of 75%, the total EAV of these parcels would be $428,268, for a net increase of at least $392,772. (I say “at least” because some or all of the class 239 parcels may be assessed at less than $150 and therefore completely untaxed.) The latest report I can find for Ford Heights total EAV, from 2022, is $14,201,062. Thus, if my assumptions are correct, and tax levies don’t change, then the typical property owner would save just 2.76%, Longer-term, landowners might be encouraged to develop their parcels, with housing or other improvements, so the benefit over time might be greater and might not only be financial. There would be no expense to the Village or other taxing bodies.

And of course the captioned illustration at the top of this post, 7+ acres in desirable Hanover Park, easy walk to Metra, adjacent to residential areas (or suitable for retail/commercial use), takes advantage of class 239 to pay taxes of less than $200/year.

The current locally assessed value of these 59,886 parcels totals $490.23 million. By ordinance, these assessments are 10% of what the Assessor estimates to be the market value of these parcels, implying that they’re worth $4.902 billion. Of course there’s also a “multiplier” of 3.0163, meaning the taxable value is $490 million X 3.0163 =$1.478 billion. Tax rates vary around the County, but in Chicago currently (before expected increases) is 7.02%. Meaning that owners of vacant land need to pay $1.54 billion X 7.02% = $103 million.

The County Board decided that vacant land, like residential real estate, should be assessed at 10% of estimated value. Commercial and industrial land is assessed at 25% of value (with exceptions for special favors). The Board could, by ordinance, apply this 25% factor to vacant land also. Which would raise something like $490 million X 1.5 X 3.0163 X.0702 = $155 million/year. Without taxing any housing; without taxing any business. Without taxing anybody who can’t afford to own land. Now $155 million may not seem like a lot, given that the City of Chicago is running something approaching a $1 billion annual deficit, Chicago Public Schools hundreds of millions more, and of course many suburban Cook County taxing bodies are in deficit. But $155 million is just the start.

If you are owner of a vacant lot, and you receive notice that your taxes have more than doubled, what will you do? You could sell the lot, but who would buy it? Probably somebody who wants to build housing, or a commercial business, or something else that serves the community. Or you might decide to build something yourself. Either way, this contributes to better housing supply or increased job opportunities.

Also, that $155 million/year is just for actual vacant lots, coded by the Assessor as class 100. There are also 25,180 parcels labeled as “vacant land under common ownership with adjacent residence” (class 241), also assessed at 10%. These are assessed at $123 million. By the same calculation as we used for vacant lots, assessing these like other nonresidential property could yield an additional $39 million, and some of the parcels would be used for new housing (including accessory dwelling units) or other useful projects.

This amount of revenue is not going to solve all the financial problems of Cook County local governments, but it would be a start, would cost practically nothing to implement, and would have the side benefit of increasing jobs and housing.

Many vacant lots are not taxable, because they belong to the City of Chicago or other government agencies. The above calculations omit such lots. DePaul’s Institute for Housing Studies has examined vacant land in Chicago, including City-owned parcels, and provides some analysis here.

This is not a complete remedy for Chicago’s and Cook County’s financial (and other) difficulties. But it should be an element in any plan to achieve prosperity and justice.

“Cook County assessor misclassifies hundreds of properties, missing $444M in one year alone,” says the Chicago Tribune. The report is joint with Illinois Answers. $444 million is a lot of money, about 1/2 of 1% of all the assessed value Countywide. And assessment data is public, so the journalists could easily find examples of inconsistencies.

Evidently, Fritz didn’t do as good a job as we wish. The journalists didn’t report any comparable error rates for other jurisdictions; perhaps they couldn’t find any. Some Cook County taxpayers were unpleasantly surprised when, the Assessor having suddenly discovered their improvements, they received big bills for back taxes.

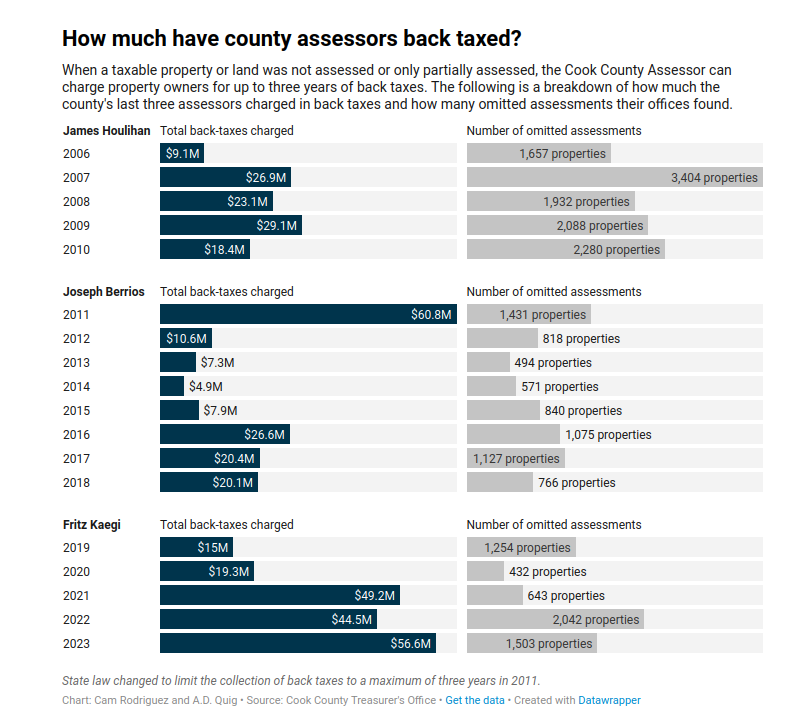

The report includes a chart showing annual number of improved properties discovered and amount of back-taxes billed for each year going back to 2006:

From the Chicago Tribune / Illinois Answers report.

From this it appears Fritz’s record is pretty much in line with the results of prior Assessors. He says there are 1,864,161 taxable parcels in the County, so in his worst year he discovered missed improvements on 0.1% of them.

Note that the Tribune/IAP folks mislabeled the chart; the assessments probably weren’t “omitted,” but the properties were underassessed because improvements weren’t recognized.

The report includes a number of complaints by former County employees and some local officials, essentially agreeing that Fritz did an imperfect job. There’s even a time-series of aerial images of a subdivision in Lynwood, showing very clearly that houses have been built, but didn’t yet show up on the tax rolls. For a village of 9116 people, and their school districts, this subdivision of a few dozen houses might be a significant fiscal consideration. And for the new homeowners, the back taxes will be a burden.

(The report implies that in this case the ball was dropped by the Bloom Township Assessor, an intermediary between Fritz and the municipality. )

The journalists also start, and conclude, their report with the case of one property owner who has experienced serious tax increases and is considering moving out state. Yes, excessive and wasteful government spending, and high taxes, is a big problem here. But fixing assessment errors affecting 0.1% of the parcels will do little to address it.

We could make a couple of observations here.

What if Cook County could drop improvements from the tax base, assessing and levying only on the value of land, what the each parcel would be worth if vacant? Probably none of the problems described in this report could have occurred. And instead of increasing “the number of budgeted field staff from 34 in 2023 to 38 in 2024,” Fritz could have laid off most of the field staff, putting a few to the task of correctly valuing land. He’ll also need (probably already has) somebody to monitor the County Clerk’s Tax Map Department, to be sure parcel boundaries and numbers are up to date.

How does the government’s ability to accurately administer the property tax system compare to the income tax system, or the sales tax system?Nobody knows. While nobody really understands how income taxes work, the revenue agencies release only aggregate data, so we know nothing of any invidual’s situation unless the person chooses to publish her income tax returns, as some politicians do, or somebody violates the rules and liberates confidential information. Even sales tax information for individual taxpayers is largely confidential. To guess how well these taxes are administered, one could search for /IRS agent indicted/ on luxxle or freespoke .

And here’s a report asserting that over a recent 18-month period, more than 1% of Internal Revenue Service employees had “confirmed tax noncompliance issues.” (Apparently most of them kept their jobs.) If 1% of IRS employees are “cheating,” I doubt that the percentage for average taxpayers is less. So it seems that overall, Fritz is doing a better job than the Feds.

Maybe he should ask the State to make his job easier by removing improvements from the real estate tax base.