We have a Libertarian Party candidate for Cook County Assessor who apparently hasn’t learned the lessons of California’s Proposition 13. So he wants to do something similar here. Too late to do anything about that, I suppose, so this post is aimed at anyone thinking about running for Assessor in 2030.

The candidate proposes to “limit property taxes to 1% of assessed value with annual inflation increases capped at 2%.” In fact, the Assessor has no power to set property taxes, and is required to assess property at a predetermined percentage of his estimate of its market value. Changing that would require action from the State Legislature, and probably also the Cook County Board.

An Assessor candidate seeking tax reform might be successful with a different proposal: Simplify assessments by excluding all buildings and other improvements, taxing only the value of the land as vacant, and gradually increase the tax rate to eliminate the need for sales tax, income tax, and other prosperity-killing taxes. Of course this would also require cooperation from the State and County, but at least it would remove the burden on production, reducing the cost of living (including housing) and encouraging entrepreneurs who hire people to do useful things.

This 2030 Assessor candidate would need to improve the assessment of land value (assuming that the prior Assessor hasn’t done so) to realistically reflect what each site is worth. Then Cook County can move toward a true libertarian tax system. The Ultimate Tax Reform.

The wildfires aren’t completely controlled at this writing (January 15), but they will be. Estimates of dollar loss are all over the place, the highest I’ve seen is $275 billion. Maybe it’ll be more; let us suppose $400 billion is the cost to replace the buildings and other wealth that has been lost. Let us further suppose that half of that will be covered by insurance from solvent companies. Finally, let us suppose that it is public policy to compensate private individuals and corporations for their losses, even tho no such compensation is provided to victims of common thieves.

So who should pay this $200 billion? Well, the US Federal government has lots of money and can issue bonds as needed to obtain more. But it’s already over $36 trillion in debt, ignoring some big obligations. Ultimately the money will come from federal taxpayers, of whom we may assume there are about 200 million (The total number of personal returns filed appears to be less, but some are joint.) That would work out to $1,000 per taxpayer, tho of course more for those who lack effective lobbyists and less for those who don’t.

But why should this be a Federal matter at all? Why can’t the people of California, or even of Los Angeles County, cover the cost? They’re certainly closer to the situation. The County Assessor tells us that the total assessed value of taxable property in the County is $2.1 trillion. But like other jurisdictions, this involves many fictions, and the actual value of any given property is typically several times the assessed value. In California this seems to be largely due to Proposition 13.

It seems that in LA County, at least for residential parcels, the land value is typically much greater than the improvement value. [edit 1/18/25: This article and link therefrom supports the assertion that “[l]and values in Los Angeles account for an extremely high share of home value.”] What this means is that, if you bought a house and lot for $1,000,000, and the house was destroyed, you actually lost less than $500,000. Combining the Countywide underassessment with the relatively high proportion of value in land, the $2.1 trillion in total assessed value probably includes actual land value greater than $2.1 trillion. And if this value were taxed at, say 1%, it would yield more than $21 billion/year that could fund recovery and rebuilding. (This 1% would be in addition to the much lower effective rate already applied.) There is no need for Federal taxpayers to bear this burden, which benefits primarily owners of very expensive real estate.

This is essentially how San Francisco recovered from its 1906 earthquake, as documented by Mason Gaffney in this article.

Continuing our exploration of land values and real estate taxes in Cook County …

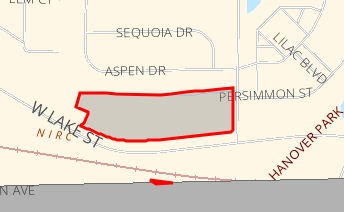

Parcel #06364020270000, at 1830 Lake St in Hanover Park. 7.36 acres, adjacent to a residential area and virtually across the street from a Metra station. Due to favors done for class 239 farmland owners, it pays less than $200/year in property tax.

The County contains 813 parcels coded as class 239 “non-equalized land under agricultural use, valued at farm pricing.” An explanation of how farms are supposedly assessed is included in this document, page 12 of which states:

The assessor notes each of the farm’s land use categories and uses the equalized assessed value for each soil productivity index to determine the assessed value. The assessor may make some subtractions for things like slope, drainage, ponding, flooding, and field shape and size before calculating the final value. • The portion on which crops are planted is assessed at the state-certified equalized assessed value certified by the Department for the corresponding soil productivity index. • Permanent pasture is assessed at one-third of what would be assigned if it was planted in crops. • Other farmland (e.g., forestland, grass waterways) is assessed at one-sixth of what would be assigned if it was planted in crops. • Wasteland has no assessed value unless it contributes to the productivity of the farm.

For Cook County, the Assessor provides specifics here.

The total assessed value of these 813 parcels is $2.25 million. To calculate their acreage it seems I would have to retrieve the records manually and individually, but the 2022 Census of Agriculture says the County contains 154 farms totaling 10,281 acres. (A farm might comprise several parcels). This implies an assessed value of $218/acre. Reviewing a small sample of parcels, it appears that the Assessor values most class 239 parcels at $2250/acre, and assesses them at 10% of that, or $225/acre.

One might compare this to the Illinois Society of Farm Managers and Rural Appraisers’ report, which includes but doesn’t break out Cook County, and indicates sales prices in Northeastern Illinois range from $5500 to $40,000 per acre.

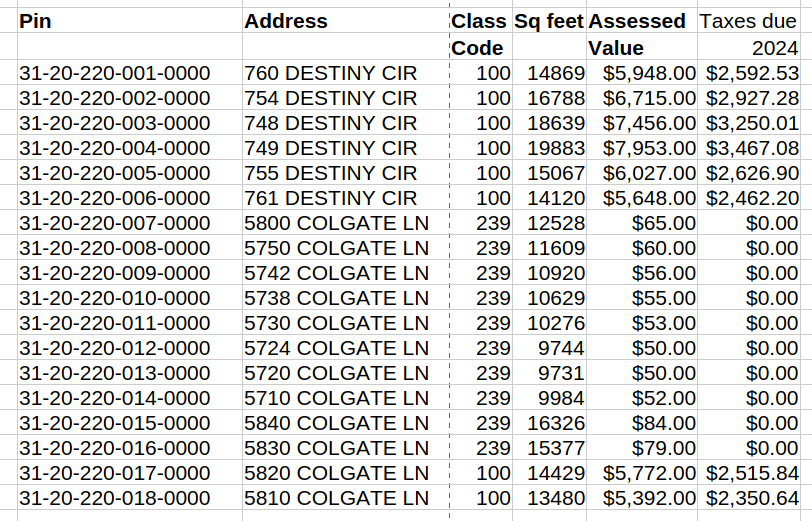

There’s no minimum parcel size for a “farm” under class 239. Thus, we have a series of 18 small vacant lots in Matteson: 31-20-218-001-0000 thru 31-20-218-018-0000. All of these appear to be empty lots, awaiting the construction of houses. Eight of them are classified as vacant land, with assessed values ranging from $5392 to $7953 (differences apparently due to differing sizes). Taxes due on these in 2024 range from $2351 to $3467 (excluding overdue taxes from the prior year, but including interest charged). But ten of these similar lots are class 239, farmland, assessed at $50 to $84. The County issues tax bills of zero for these parcels. This is claimed to be due to 35 ILCS 200/18-40, which states

If the equalized assessed value of any property is less than $150 for an

assessment year, the county clerk may declare the imposition and collection of

all tax for that year to be extended on the parcel to be unfeasible and

cancelled. No tax shall be extended or collected on the parcel for that year

and the parcel shall not be sold for delinquent taxes.

However, these parcels are assessed at $50 to $84. Applying the equalization factor of 3.0163 results in EAV greater than $150. In response to my inquiry, the Cook County Treasurer explained that, even tho equalized assessed valuation is printed on the tax bill, it isn’t used for taxation of farm properties. Here are the 18 parcels:

18 vacant lots in Matteson

I don’t know why 10 of these properties are assessed as farmland while 8 are not.

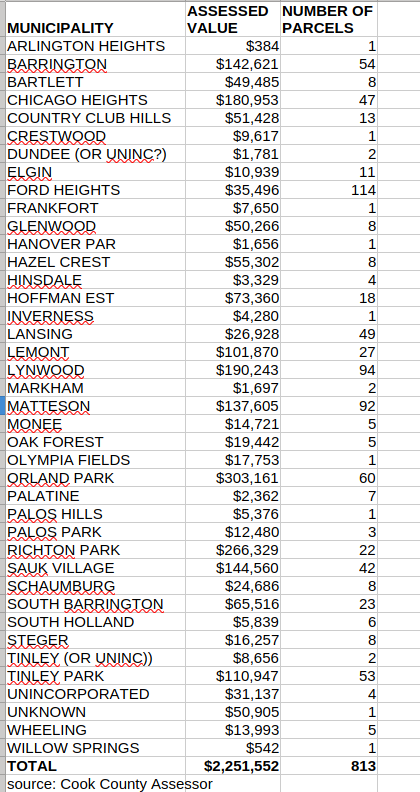

Countywide, the 813 class 239 parcels have a total assessed value of $2,251,552. While the Assessor’s records are imperfect (there being, for example, no “Dundee” municipality in Cook County), it appears that only 37 of the County’s municipalities (plus a few unincorporated areas) contain class 239 parcels. The tally is shown in the following table. Keep in mind that these are assessed value, 1/10th or less of the actual market value.

Summary of Class 239 parcels by place

While class 239 is a great bargain for owners of “farmland,” the inequity doesn’t seem, by itself, to have a major effect on the financial condition of the taxing bodies. For example, Ford Heights has the largest number of class 239 parcels, 114. Total class 239 assessed value in Ford Heights is $35,496. If this land was subject to equalization like other parcels, the equalized assessed value would be $107,067. As noted above, the Assessor seems to undervalue class 239 parcels, but even if we assume undervaluation of 75%, the total EAV of these parcels would be $428,268, for a net increase of at least $392,772. (I say “at least” because some or all of the class 239 parcels may be assessed at less than $150 and therefore completely untaxed.) The latest report I can find for Ford Heights total EAV, from 2022, is $14,201,062. Thus, if my assumptions are correct, and tax levies don’t change, then the typical property owner would save just 2.76%, Longer-term, landowners might be encouraged to develop their parcels, with housing or other improvements, so the benefit over time might be greater and might not only be financial. There would be no expense to the Village or other taxing bodies.

And of course the captioned illustration at the top of this post, 7+ acres in desirable Hanover Park, easy walk to Metra, adjacent to residential areas (or suitable for retail/commercial use), takes advantage of class 239 to pay taxes of less than $200/year.

We have an article from Crains reporting on the winning proposal for solving the disaster that is the City of Chicago’s pension plans. Of course a new fee is involved, being a toll on DLSD. Article doesn’t disclose how much this toll would be, nor its likely impact on traffic. I suspect that parallel arterials would see increased congestion, while DLSD itself might flow a lot better with reduced traffic volumes.

The two runners-up proposed income tax increases. One would be a 1% income tax on the remaining Chicagoans, to be termed a “public safety tax” and used to fund police and fire departments, freeing up municipal funds to go to pensions. The other proposed raising the State income tax to 6%.

There were originally eight proposals, and perhaps one of the losing five made the logical proposal– a tax on whoever controls on-street parking. Like any real estate tax, this would be based on the value of the control, and should be set such that LAZ Parking can retain just enough profit to operate the system. .The Sun-Times’ Fran Spielman said LAZ grossed $136.2 million in 2021).

A tax collecting most of that annually could make a significant dent in $35.4 billion shortfall recently estimated for the City’s pension funds, tho it couldn’t cover the entire need. And that doesn’t include Chicago Public Schools, Cook County, State of Illinois, and other government pension funds which are in difficulty.

All these proposals come from students at UChicago’s Harris School of Public Policy. Which somehow reminds me of the remark decades ago from Mike Royko, observing that Hyde Park isn’t really part of Chicago, but rather a sixth boro of New York.

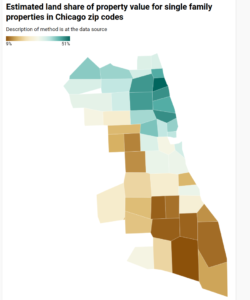

UPDATE Aug 29 2021: If anyone familiar with Chicago doubts that removing improvements from the tax base will ease the burden on low-income homeowners, this map will be instructive. The original, mapless post from Aug 25 follows.

We sometimes are told that a land value tax (LVT) would punish the poor person who has a small rundown house on a high-value lot, while benefiting the person next door who has a large fancy house on an identical lot. And that’s not wrong, it’s just atypical. In practice, we believe, poor people mostly live in neighborhoods where housing is cheap and land is cheaper, thus they would tend to benefit from a shift to LVT.

As the quality of Cook County assessments has been improving, we expect to be able to show this by analysis of that data. In the meantime, we have some estimates of land and improvement value from William Larson and colleagues at the Federal Housing Finance Agency. Using appraisals produced for mortgage underwriting, they estimate land and improvement values for homes in most zip codes (and census tracts) nationwide. Their source data includes only single family properties which were appraised for mortgage purposes. They consider only parcels where the improvement is less than 15 years old, and exclude vacant land as well as land where the appraised value is very close to the assessed value (in case appraisers might have relied on low-quality or obsolete assessments). Also excluded are zip codes with an insufficient number of single family home transactions.

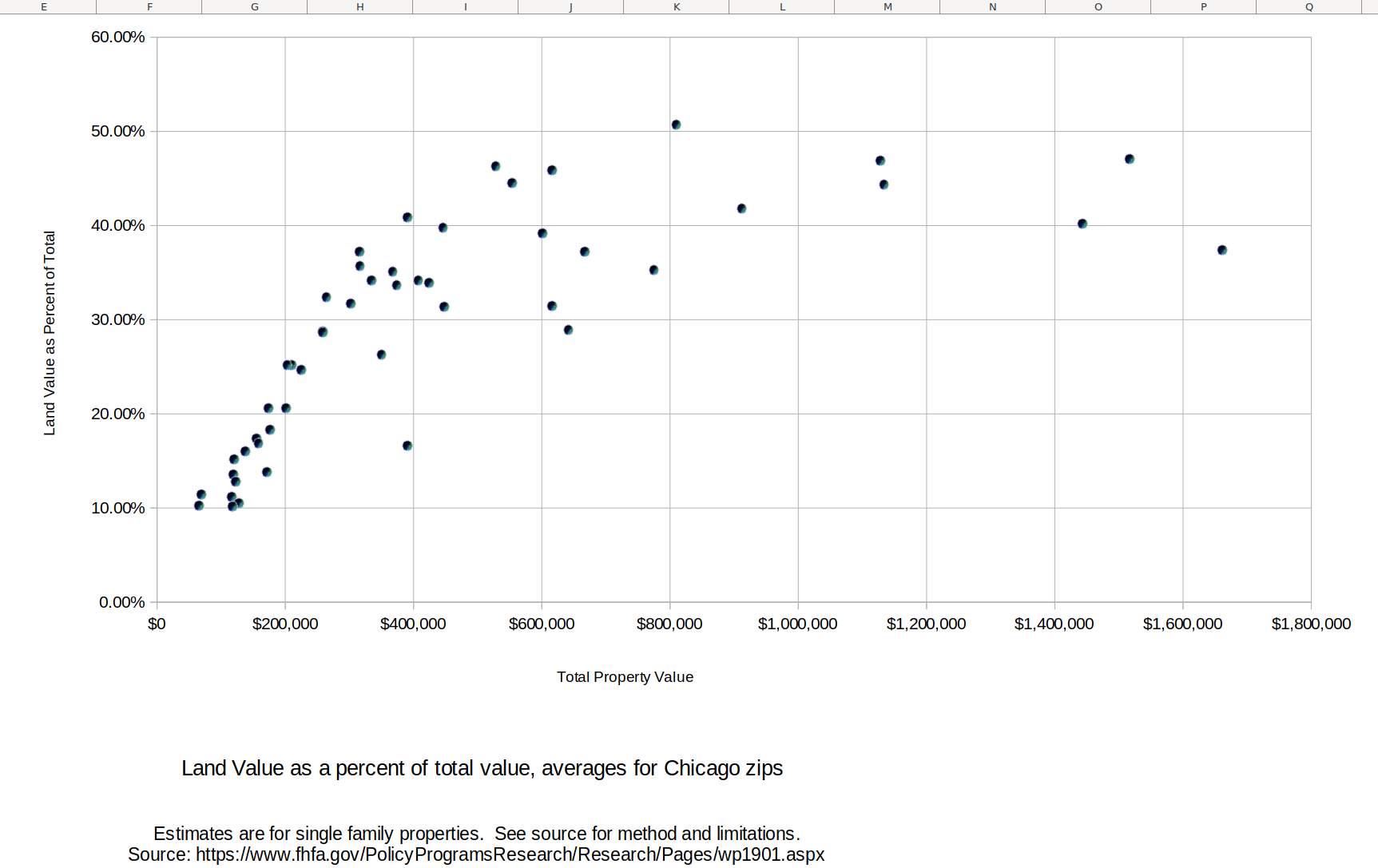

The chart below shows, for Chicago zip codes, the ratio of land value to total value (vertical axis) and total value of the property (horizontal axis. What stands out is that the ratio tends to be lower where the properties are cheaper. That is, a revenue-neutral shift of property taxation to land values only, ignoring value of improvements, would tend to reduce the taxes on low-value zip codes, while increasing it in higher-value areas.

The table below shows the data for each zip code, sorted from high proportion of value in land to low. Clearly the more affluent areas have lower proportion of improvement value, and the areas with low income population have a higher proportion of improvement value.

Estimated land value proportion and related data for single family properties in Chicago zip codes

Also of interest, even tho the low-value areas have a high ratio of improvement to land value, this isn’t because of large houses on small lots. The floor area ratio is generally lower in the areas with lower land value proportion.

Overall, the above data is consistent with Georgists’ assertion that low-income residents usually benefit from a switch to LVT. I might be taking a further look at this dataset.

Where fairness comes from: Cook County Board Pres. Toni Preckwinkle; Illinois House Speaker Michael Madigan (credit: WBEZ CC BY-NC 2.0 and Wikipedia)

We have a new North Suburban Reassessment Report from Assessor Fritz Kaegi. As a “reformer,” this Assessor publishes a lot more information than his predecessors. In fact, he publishes all the code for his assessment models.

Accurate assessments are said to be important because assessing a property too high can “destroy wealth by diminishing the market value of the property.” Which is true, but do not taxes based on accurate assessments also destroy wealth? What the Assessor seems to mean by a “fair” assessment is an assessment that is calculated in accordance with applicable laws and ordinances. This definition of “fair” comes mainly from our friends in the Legislature and County Board, with some role for other government officials. “Fair” in Cook County means that owners of houses or vacant land should pay taxes at 40% of the rate applied to ordinary industrial or commercial property, unless special favors have been bestowed. In the rest of the State, “fairness” requires rates in the absence of special favors to be uniform. In all areas, “fairness” requires that religious and most nonprofit educational facilities are entirely exempt from tax. Continue reading Clobbering fairness more accurately

I was only a bit surprised to find that Chicago’s 2020 police budget is $1,778,002,408, or $660 for each of the 2,693,976 folks that DJ Trump’s Census Bureau estimates live in Chicago. This doesn’t include $737.5 million for the police pension fund, nor $204,867,834 for the Office of Emergency Mgt and Communications, nor $135 million for “judgments and settlements against the City,” (including but not limited to police misbehavior), nor the police-related portion of the City’s capital budget, which seems to include the “joint public safety training academy” ($85 million, but just $15.75 million in the current year), and some other facilities. All told, and without doing the detailed analysis which I wish the Civic Federation would do, it seems the the City spends something like $1000/person/year for police. That doesn’t necessarily mean that police should be defunded in whole or in part; after all, reported crime has for the most part been declining, so perhaps we are getting something for our money. But it gives some idea of the dollars involved. (And it turns out that, as I was writing this, the Civic Federation produced a post covering much the same ground, with better context and detail and colorful charts, and noting that I failed to include some undetermined but substantial benefit costs among the cost of police.)

Compare police costs to Chicago Public Schools. CPS is a separate unit of government, but controlled by the Mayor and funded mainly by Chicago property tax payers. For the current year, it’s planning to spend $7.84 billion, or $2910 per Chicago resident. Enrollment continues to decline, 13% in ten years (roughly the same amount as reported crime, but that might just be a coincidence).

Summing the police and school expenses, Chicago spends $3910/person. For the hypothetical family of four, that’s over $15,000. I wonder how many two-worker households would prefer to have one stay home, help educate the children, hiring tutors as needed, and keep an eye on the neighborhood, if their income increased by that amount. Just a thought.

Update September 27: It turns out I’m not the only one suggesting that we spend too much on government schools.

Wirepoints recently issued a helpful report showing state and local government pension debt per Chicago household. They estimate the burden at $144,000 per household. This is a big number, but one could suppose that a prosperous household, over decades, could bear such a burden. Some could, but probably not those below poverty level. Take them out of the picture and the per household amount rises to $172,000. Excluding households with incomes below $75,000, or below $200,000, and the per-household amount rises further, to $393,000 and $2,022,000 respectively.

Here’s their chart:

Of course this doesn’t consider land values, nor businesses. If prime Chicago land is worth $1,000/sq ft, that’s 5.38 sq miles. But more typical land value is much less, probably no more than $25/sq ft. (it seems that nobody has tried to estimate citywide values). That would be 112 square miles. Once we subtract land owned by governments, churches and other exempt nonprofits, we might be approaching the total value of all land in Chicago. And that’s just for pensions, not bonded debt, nor needed capital improvements. Real estate buyers know, or certainly should know, about these encumbrances.

Of course money can be raised from business taxes, but that’s hardly a way to grow economic opportunity for Chicagoans. I would consider any tax revenue from “gaming” as a kind of business tax.

The lesson Wirepoints draws from this is that pensions have to be downsized somehow, which required amending the state constitution. And they go further, comparing government salaries to those of the private sector:

So it looks like we’re going to have to confront a large number of people with guns and firehoses and control over our children, who have been getting a lot of money from us for years and may prefer not to moderate their demands.

Tho I don’t know how, this problem will be solved. Maybe MMT will yield a continuing stream of funds to bail us out. Maybe inflation will accelerate such that the fixed 3% compounded pension increase isn’t a burden. Maybe Chicagoans will decide that they just don’t want so many government “services.” Maybe politicians will decide to remove all taxes from productive economic activity, taxing only the value of land and other privileges (such as the private monopoly over street parking fees), which will grow the economy (while reducing the need for emergency services) sufficient to make pensions a non-issue.

And when it is solved, those who own land and other privileges will benefit most.

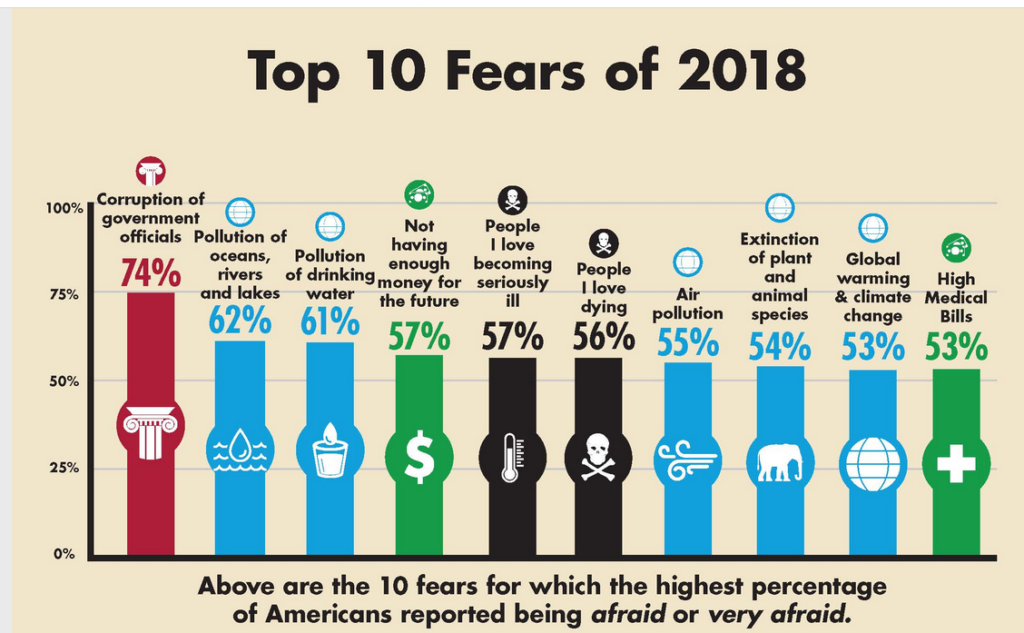

source: Chapman University Survey of American Fears

I don’t know that governments are always and inevitably corrupt, but there sure seems to be a lot of corruption going on. It isn’t a new development; maybe it’s worse nowadays or maybe just more visible.

So how can we single taxers say that we want the government to collect all, or nearly all, of the economic rent? Don’t we know that it will be stolen or, at best, wasted?

Not necessarily. Consider the following:

In the U S at least, real estate tax is administered and collected at the local — that is, substate– level. This is where the records and expertise needed to operate a land value tax exist.

Unlike income tax or sales tax, nearly all the data involved in real estate taxation is public information. Most of this data is accessible to everyone with internet access, generally without fee. I can see how much real estate tax my neighbor paid. I cannot see how much income tax they paid. The same goes for sales taxes and most other kinds of taxes. So cheating in real estate tax can be seen. That doesn’t mean it will always be impossible for people to cheat, but it provides a much greater possibility that cheating will be observed and rectified.

Government corruption seems to be a function of government size. A survey earlier this year found that “87% of voters nationwide believe corruption is widespread in the federal government. Solid majorities believe there is also corruption in state (70%) and local (57%) government.” Looked at the other way round, only 13% of us believe the federal government is possibly honest, compared to 30% for states and 43% for localities. I actually believe that one of the local governments to whom I pay taxes is pretty honest and efficient.

State and federal governments might logically collect some of the economic rent. Examples currently include severance taxes and could reasonably include rents for electromagnetic spectrum should our rulers become persuaded to levy and collect them. Existing federal agencies are able to review and evaluate collection efforts.