Selection from Olcott’s Land Values Blue Book, 1936 edition, Numbers represent values per front foot, to be adjusted as described in the book.

Assessor Fritz Kaegi appears to seek assessments that are more consistent with applicable laws and ordinances, and easier for taxpayers to understand. This might be a good thing, tho one hopes that, once taxpayers understand how assessments are done, they’ll demand a more helpful system, one which doesn’t punish homeowners and businesses for building or improving.

As Polly Cleveland continues her project posting Mason Gaffney’s works, we find “Chicago’s Growth Spurt, 1890-1900.” It’s not very long, and worth reading today as a contrast to our current stagnation. Most importantly, Gaffney deduces circumstantial evidence that during the era of growth, land values were significantly taxed. As he notes in conclusion, “More research into Chicago’s political history is needed.”

The whole trove contains dozens of working papers, class notes, and publications, in Gaffney’s concise and understandable style. (You’ll find it linked here as well as above; depending on your screen size and magnification you might need to scroll over to the right to see it.)

Jeff Smith has provided some interesting ideas for achieving geoist progress, and enumerated a bunch of them in a February 15 2018 email to many geoists with subject line “Re: LT: Re: Trump Infrastructure Plan Calls for Value Capture Financing“. Previously and subsequently, Jeff has suggested that geoists should act in accordance therewith. Possibly because of the subject line, or the nature of internet discussions, some of us may have forgotten or never seen this message. Jeff’s text is reproduced below:

Never forget reading is part of the problem. Doing is part of the solution.

The fact that I’m the only Georgist with the curiosity to research what’s known about social change is a very telling fact. I should not be your gatekeeper to this world of fascinating information. Every or at least dozens of

people with the dream of changing society should want to know how society changes!

To not want to know is a constant reminder that I’m a member of a mad species — just like most people don’t want to know how to make economies work right.

Here are some efforts of others who know paradigm shifts follow principles:

Kuhn is the classic. “Old minds don’t change; they just die out, replaced by young open ones.” So appeal to the young. Learn to dance, you stiff fuddy-duddies. Our problem: Georgist elders attract youth exactly like themselves—conservative, conformist, obedient, not your classic profile for agents of change. https://www.ted.com/talks/derek_sivers_how_to_start_a_movement

Lakoff, one of my grad school contemporaries, is also ignored for urging do-gooders to learn how to frame: “Frame yourselves before others frame you.” You framed yourself as a taker (taxist), not a sharer, like basic income, which has far more innate appeal: https://medium.com/indivisible/george-lakoff-on-indivisible-36931ee03c5

But don’t limit yourself. Google. Yet balance mere reading with actual doing.

I have my own that worked to start several cutting-edge groups: How to Make a Movement in 5 Easy Steps:

1 Message

2 Members, including celebs

3 Money

4 Media, including star power

5 Maintenance—every other meeting should be a party. Seriously.

6 aMass the Multitudes—demonstrate—and Meet the Minions of the Moguls—i.e., lobby.

7 Make Merry your victory

Georgists fail at Step 1, so they can’t get out the gate. They must redo Step 1 and translate their message into the language of their intended audience. To know what to say, they’d have to use focus groups, polls, and surveys. But that’s too rational for ideologues, so far.

“We cannot become what we need to be by remaining what we are.”

You can’t reform by conforming. You just lose the respect of both reformers and conformists.

If there is a mistake to be made in shifting paradigms, Georgists have made all of them.

Thanks, Fred, the opportunity to feel nostalgic for old, ignored, powerful ideas. You did not offer to quit doing what does not work and devote that time to doing what does work. Hence, most likely, you asked me to waste my time.

“The dog barks but the caravan moves on.” Into the desert.

I should stop barking now.

Jeffery J. Smith Author, Perfect Timing. 503/568-5889

Crains reports today that rising land costs, as well as increases in construction costs and uncertainty about real estate taxes, is slowing construction of single family housing on the north side. One might think this would result in lower land prices, but a builder is quoted as saying lots in Lincoln Park and Lakeview, which recently sold in the $700,000 range, are now going for $900,000 and up. This makes it difficult or impossible to build a new house selling for the $1 to $1.5 million that buyers seem willing to spend.

So if it’s not demand for houses, what is driving up the price of land? Possibly more multi-family is being built? Or other uses? (Other than the City’s massive database — which doesn’t specify type of structure nor how many units, except as inconsistent text fields — I can’t find any statistics on housing construction within the City. Must be somewhere…)

Or possibly the supply of vacant lots, or deteriorated structures on lots that could be made vacant, has depleted? Or purchase and sale of vacant lots is used to launder money?

The article also notes that land costs are much lower in an isolated part of Bridgeport/Chinatown, specifically Throop & Hillock, where a recent development of attached and detached houses paid $55,300 per unit for land.

Total value of land and buildings for the 72,651 farms in the state was $196,542,978,000. This amounts to $2.7 million per farm, and $7,278 per acre. Real estate taxes paid were $431,625,000, implying an effective tax rate of 0.22%.

58% of the acreage is tenant-farmed. However most (44,378) of the farms are owned by the operator, whereas 6,021 are farmed by tenants. The remainder (22,252) combine owned and rented acreage. The rent may be cash, or a share of crop, or other arrangement. Cash rent was reported to total $1,956,402,000.

Remember that whereas Georgists are concerned about who receives land rent:

The above figures may be mostly land, but do include buildings

Even farmland may have some improvements, for example drainage tiles, and the value added by these is not “land” for purposes of political economy.

Illinois contains 7,992 very small farms of 1-9 acres (Anything smaller than 1 acre isn’t counted in this census,) Most have less than $2500 revenue, but 64 of them report $1,000,000 or more. 3122 are operated by people who say farming is their primary occupation.

The report contains a huge amount of detailed information gathered from farm operators. That may help explain why the actual response rate (nationally) was just 71.8%, with systematic estimates covering the remainder. This rate is down from 74.6% in 2012, and 78.2% in 2007. Much of the data is reported at the county level as well as statewide.

Here’s a brief paper (pdf) by two Berkeley economists suggesting how a “progressive wealth tax” could work. They assume a 2% rate would be applied to wealth in excess of $50 million per household, or maybe $25 million per individual. Most of us, then wouldn’t need to pay anything. The only question for the authors is the practicality of such a tax.

I was surprised to discover that, according to the paper, wealth taxes already exist in Switzerland, Spain, Denmark, and Sweden. References are cited indicating pretty good compliance, the lowest being in Switzerland (where the authors find the estimated 23%-34% evasion rate “not as compellingly identified as the other estimates.”) I didn’t review the cited papers to learn the details of how the compliance was estimated.

They note that wealthy people can hide their assets abroad, but imply that they could be caught if the government had more resources. While it’s possible for the wealthy to avoid some taxes by leaving the US and renouncing citizenship, the proposal includes a 40% tax on the wealth of the departers. They praise FATCA and recommend it be more vigorously enforced, without considering the disruptions it’s already caused (pdf) for many Americans who live or work abroad.

They aren’t concerned about the wealth tax reducing the availability of capital goods for productive use in the US, because they assume any decline in investment by Americans could be made up by foreigners, by the less-wealthy, or by government expenditures funded by the wealth tax. They don’t address the issue of what percentage of “investment” is actually productive.

They also don’t worry that the wealth tax would reduce innovation, pointing out that most innovation is done by people with less than $50 million, that innovation is enhanced by providing children with exposure to it, and that the wealth tax might encourage the rich to invest in more productive ways. Again, they aren’t concerned about the extent to which “innovation” is a good thing.

They don’t believe the wealth tax would discourage talented people from immigrating, pointing out that the government imposes lots of barriers to immigration which it could adjust if needed.

As for the impact on charitable giving, they curiously suggest that “foundations used to shelter wealth (i.e., controlled by wealthy individuals and not used for charitable purposes) should be subject to the wealth tax.” They don’t explain how such foundations could be identified, and why they are currently tax exempt.

The scariest part of the paper regards “information reporting.” They point out that the IRS already requires extensive reporting of income and, to some extent, assets. These would just need to be modified to better report wealth. Of course this means that everyone’s assets and liabilities needs to be reported, if only so the rest of us can “prove” that we don’t have enough net assets to be subject to the tax. For real estate, by the way, they assume that local assessor records would be an adequate source. They don’t address the problem of offshore secret trusts. They indicate no interest in counting “intellectual property”

Many years ago, an anonymous former IRS agent wrote a book advocating a “Doomsday Machine,” which would record every financial transaction by anyone in the US (and presumably by Americans abroad, I don’t recall.) He thought this was the only way that the income tax, as it existed then, could be enforced. Of course, since that time, this kind of surveillance has been facilitated by the digitization of much of the economy. It the book were updated, he’d now have to expand his machine to include all kinds of assets and liabilities.

Just in case anybody read this far and missed the point: A tax on the value of land, other natural resources, and government-protected privileges would avoid nearly all of the above problems, while still falling mainly on the wealthy.

update February 26 2019– NPR reports more poor results from wealth taxes, tho they don’t completely write them off.

Taken from Henry George, the title of this post refers to economists who make good points but don’t get to their logical conclusion. Mariana Mazzucato may be another. We may start by looking at some of the main themes of her book.

Value extractors are obtaining a large and increasing share of wealth produced, resulting in a smaller share for those who actually produce valuable goods and services. This problem has several interlocking causes.

Measures of national product (GDP) conceive value as equal to price, meaning that any profitable activity adds to national product even if it’s essentially an extraction of value rather than production of good or service of value. In recent decades, opportunities for private value extraction have multiplied.

One effect of this increase in private value extraction is that the extractors now have effective control of much of the government. Lobbying by value extractors changed national income concepts to include their extractions in GDP.

Further, the conventions of national income calculation tend to understate the value of government work. This is because the value of a private company’s production necessarily exceeds, on average, the cost of labor and capital inputs (otherwise the company would have no profit). A government’s production, by contrast, is treated as equal to the cost of the inputs, even if the value of the product is much greater.

Partly as a result of this undervaluation, some services previously provided by government have been “privatized,” which means, in most cases, are still funded by taxes but are performed by employees of private firms under contract.

Some examples of the

problem:

As retirement income becomes based on earnings of assets, pools of assets grow and opportunities for value extraction multiply. This includes fees for managing investments, and various side-hustles.

As governmental functions are “privatized,” the quality of service drops along with the earnings of people who provide the service. But costs typically don’t decline because of contractors’ profits and lobbying expenses.

Patent privileges have been vastly expanded in recent decades. This provides more opportunities for value extraction, but actual useful innovation seems to be retarded by patents. Also, as patent offices have become understaffed relative to the workload, patents become easier to obtain.

Governments (or their banker overlords) seek to reduce the deficit/GDP ratio by reducing spending, failing to recognize that some kinds of government spending actually facilitate an increase in GDP far in excess of their cost.

The dominant neoclassical economic ideas assume that rent can be competed away, and that unemployment is voluntary. They further fail to recognize “the collective and cumulative processes behind innovation.”

The remedy? According to the author:

“We” need to “define and measure” the “collective contribution to wealth creation,” to overcome the “price=value thinking…” and recognize that most of the “…creation of value is collective.”

“We” should also recognize that the current structure of corporations, controlled by shareowners thru boards, with no formal role for employees, customers, and other “stakeholders,” is not the only possible or practical way to arrange things.

The role of governments, as well as nonprofits and cooperative organizations, in value creation needs to be recognized.

Tax laws need to be modified to advantage actual value creators rather than value extractors. In addition to changes in income tax laws, a small tax on financial transactions would be helpful.

Patent laws need to be modified to discourage abuse. To encourage particular kinds of innovation, bounties might be substituted for patents.

Portraying government as “investing, not spending, can eventually modify how it is regarded.” [of course this little trick has been used by U S politicians for many years.]

“We” need to develop a vision of what society needs, and set government priorities regarding infrastructure, services, and regulations to achieve it.

So what is the value

of this book?

It does give some history of concepts of national income, going back to the 17th century and summarizing views of William Petty and Gregory King as well as Adam Smith, the Physiocrats, Ricardo, and (with special admiration) Marx and Keynes. It does discuss rent, mostly in an accurate way. There’s no mention of Henry George, perhaps because this part of the book is euro-centric, or perhaps for other reasons. She does mention some important Americans, including Elinor Ostrom.

It identifies the problem of accumulated privilege, resulting in value extraction, which impedes real progress.

It clearly describes some principal means by which value is extracted.

It taught me a few things about the way GDP is calculated, and the history of patents.

It clarifies that there’s nothing “natural” or “inevitable” about the way our economy is set up; many different arrangements for such components as corporations and patents could work, and some would be a lot better than what we have.

In a description of VW and the “dieselgate” affair, she acknowledges some of the limitations of her proposals.

As a Georgist, I see

two big shortcomings with this book:

(1) Even tho nowadays the value extractors have effective control of governments and other powerful institutions, the author seems to assume that somehow these forces will be overcome once the people come to understand that government really is useful, and that the benefits it provides are far greater than is reflected in GDP. Furthermore and related, there is the assumption that the bulk of government expenditure is good, that government is for the most part honest and reliable. There is also almost no mention of the huge waste on military, punishment, and other expenditures which an honest and efficient government would need to eliminate. So, once proper understanding is achieved, the government will wisely set priorities and provide appropriate infrastructure and services. No method is proposed for accomplishing this, and the alternative of decentralization really gets no attention.

(2) While rent is mentioned, and for the most part correctly characterized, there’s no discussion of how rent can be used to properly fund services and eliminate other taxes. It’s true, of course, that some privileges are best eliminated, but for use of real estate parcels, electromagnetic spectrum, and other natural resources the wise policy in most cases is to allow private ownership but collect virtually all the rent for public use.

And then there are a

few little nits to pick.

She does not like corporations to distribute profits to shareholders. Partly this seems to be because share buybacks are one of the several ways that corporate management contrives to reward themselves excessively, but also she displays a fundamental belief that corporations should reinvest in their business, apparently without regard for whether management believes worthwhile opportunities are available.

“A recent study by researchers at the University of Pennsylvania…” is referenced on page 219, but without footnote or citation.

On page 44 she describes rent as including “what you pay a landlord to live in a flat.” This is inconsistent with the way she uses the term elsewhere in the book, since only part of what you pay to live in a flat is to cover the proportionate share of the land it occupies; much is for use of the structure (capital) and services (labor).

In conclusion, this is a pretty good book for understanding how some means of wealth extraction work and why it poses a danger to the rest of us. It encourages us to consider alternative ways for organizing our communities. But it’s weak on practical solutions.

additional note: Mariana Mazzucato has recently been interviewed regarding this book on Econtalk and Alphachat.

another additional note: Font sizes may appear a bit screwy herein because I haven’t figured out how to enlarge the teeny font that seems to be the default in WordPress lists under the new Gutenberg editor. Someday maybe I will.

Good reporting from Wirepoints, based on articles from Reason and Pro Publica, about the City of Chicago pushing low-income motorists into bankruptcy. These sources focus on the twin injustices of punitive ticketing and fines, and aggressive impoundment of innocent motorists’ cars. Of course parking restrictions, liability insurance requirements, and traffic rules need to be enforced, but it’s pretty clear that Chicago Police and other municipal actors see this as a source of revenue to pay their salaries and pensions, more than as an enforcement mechanism. The statistics imply a racist motive as well.

But that’s not the point. The point is, why do people with low incomes need to own cars? Why can’t they get where they need to go by transit? The answer, of course, is that in most affordable neighborhoods transit is sparse: Buses run slowly and infrequently, and quit early. Rail is only a bit faster, and most lines also lack 24-hour service. Relatively few jobs are reliably accessible within an hour, or even two hours travel time. And with the demise of neighborhood retail, cars are almost essential for shopping. Schools, libraries, other government facilities have large free parking lots even it they’re poorly-located for transit and pedestrian access. So of course people who can’t afford to own and operate automobiles find they’re compelled to have them.

This doesn’t justify the municipality stealing money and property from residents already living on the economic edge. It just makes it worse.

Christopher Flavelle’s recent Business Week article looks at how rising sea levels can affect ownership of newly-submerged land. Part of the problem, of course, is that owners of these parcels want the government (Corps of Engineers, local authorities, somebody!) to use expensive artificial means to preserve or recover their properties, but of course don’t particularly want to pay for the service. Complicating the situation is the public trust doctrine, as applied in the various coastal states, which prohibits private ownership of submerged land. So if the land is recovered, who owns it?

A land value tax won’t prevent land from being submerged, and won’t clarify ownership, but it will importantly change the incentives. The article cites one case where the landowner continues to pay real estate tax [presumably a modest amount, but the article does not say] on the submerged parcel. ‘“It’s Gulf-front property,” says Levenson, who now lives in Tennessee. “Someday it will be valuable.”’

Suppose, instead, that the rental value of land was the sole source of public revenue. The land might someday be very useful, and might have a large rental value, but could never be sold for a high price. End of controversy. The water rises, the owner avoids the taxes by relinquishing the land. Unless the rest of us are obligated to pay to enrich a few coastal owners, this is the just and efficient way to proceed.

We have a new report(pdf) today from the Civic Consulting Alliance, pointing out that residential assessments (excluding condominiums and large apartment buildings) done by Joe Berrios and his crew are of poor technical quality, don’t make effective use of modern techniques, and tend to treat expensive properties more leniently than less expensive ones. The Tribune article gives pretty good context and describes the contents of the report, so I won’t try to duplicate it. Rather, I’ll focus on just a few things that caught my eye.

The study uses data that apparently has never been made public. That is, it belongs to the public as represented by Joe Berrios, but the public hasn’t been permitted to see it. And we’re still not permitted to see it. In fact, the consultants and the Assessor seem to have spent more than two months negotiating a five-page nondisclosure agreement (reproduced at the end of the report) to make sure we wouldn’t see it. But we are able to see some detailed analysis, in the study appendix, that’s more useful than the raw data for understanding how assessments actually work.

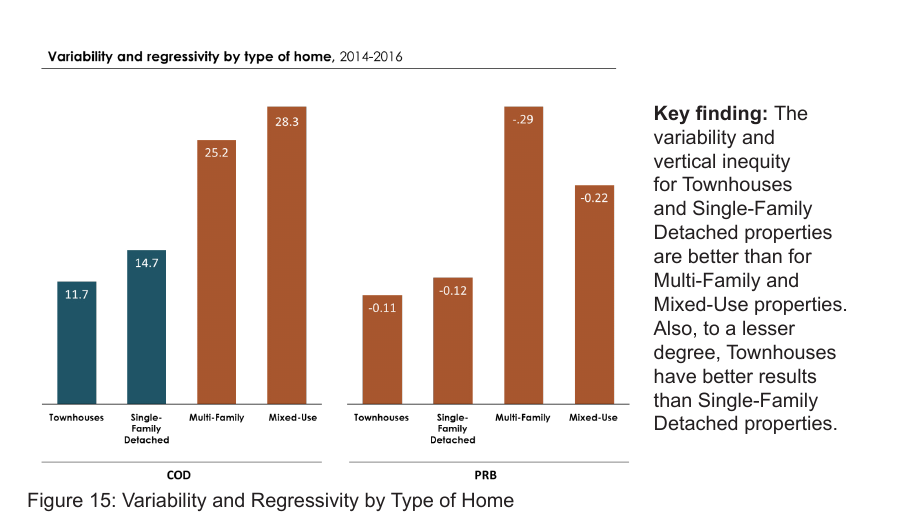

We get some useful detail on the bias in favor of expensive properties.

The above figure, which is Appendix Table 5 in the report, shows the inaccuracy (left half, shorter bar means less inaccurate) and bias in favor of expensive properties (right half, shorter bar means less bias). We can see that the bias in favor of expensive properties exists for all four categories, but is most serious for multi-family and mixed-use (residential with a storefront, for example). But for such properties, there’s no reason to expect that the expensive property contains the wealthier taxpayer.

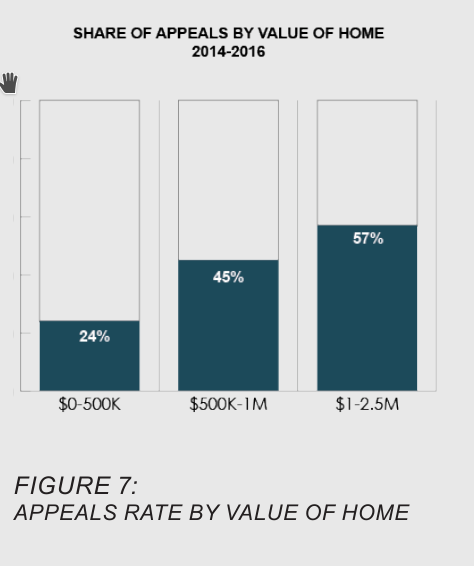

Also as previously observed, the report notes that more appeals are filed by owners of more expensive properties:

This implies that wealthier homeowners are getting a bigger tax break, proportionally, than less wealthy homeowners. I suspect it’s true, but I really don’t see any way around it within the current assessment system. The wealthier homeowner has more to gain from a successful appeal (or, what is the same thing, more to lose by failing to appeal.) She may also be more comfortable dealing with government officials and forms (and perhaps with the tax lawyers who send mailings to homeowners).

But isn’t the same true of the income tax? The wealthier taxpayer is more likely to know, or learn, tax-avoidance tricks, and/or to use a skilled tax preparer. The difference is that parcel-level assessment data is, to some extent, public information, but income tax returns in the U S no longer are.

Of course the main remedy for problems of inequitable assessments comprises:

(1) Assess only land value, ignoring the value of any improvements on the parcel.

(2) Post the assessments, including all information used to calculate them.

_(14596109179).jpg)

{kind=link}