CTA locks down Red Line extension funding, reports the Sun-Times. Contracts have been signed, and apparently the thing will be built, despite availability of a much cheaper and sooner alternative.

Sun-Times reports the total cost of the extension to be $5.75 billion. CTA say it’s 5.5 miles long, so that works out to about $16,500 per inch. They say it’ll handle 40,000 rides/day, which, allowing for weekends and holidays and maybe a scamdemic or two, comes to about 12 million rides/year. If it lasts 50 years, that’s 600 million rides. So that’s $5.75 billion/600 million, or about $9.58/ride.

image credit: Raed Mansour CC BY 2.0

Assuming the forecasts are correct.

Service is already available in this area, from Metra Electric and CTA and Pace buses, but it might not be as fast(?) and convenient as a Red Line extension would be. But my question is, if you told everyone affected that, instead of riding an extended Red Line, you would pay them$9.58 to ride a bus or Metra train, how would they respond? Over 220 workdays/year, that’d work out to over $21,000. Enough to buy and operate a car, I suppose.

Recognize, too, that $5.75 billion is only the capital cost. It doesn’t pay the train operators, customer assistants, maintenance staff.

Continuing our exploration of land values and real estate taxes in Cook County …

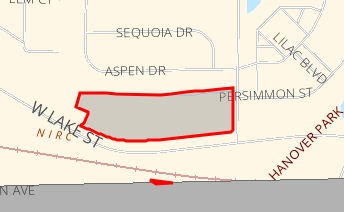

Parcel #06364020270000, at 1830 Lake St in Hanover Park. 7.36 acres, adjacent to a residential area and virtually across the street from a Metra station. Due to favors done for class 239 farmland owners, it pays less than $200/year in property tax.

The County contains 813 parcels coded as class 239 “non-equalized land under agricultural use, valued at farm pricing.” An explanation of how farms are supposedly assessed is included in this document, page 12 of which states:

The assessor notes each of the farm’s land use categories and uses the equalized assessed value for each soil productivity index to determine the assessed value. The assessor may make some subtractions for things like slope, drainage, ponding, flooding, and field shape and size before calculating the final value. • The portion on which crops are planted is assessed at the state-certified equalized assessed value certified by the Department for the corresponding soil productivity index. • Permanent pasture is assessed at one-third of what would be assigned if it was planted in crops. • Other farmland (e.g., forestland, grass waterways) is assessed at one-sixth of what would be assigned if it was planted in crops. • Wasteland has no assessed value unless it contributes to the productivity of the farm.

For Cook County, the Assessor provides specifics here.

The total assessed value of these 813 parcels is $2.25 million. To calculate their acreage it seems I would have to retrieve the records manually and individually, but the 2022 Census of Agriculture says the County contains 154 farms totaling 10,281 acres. (A farm might comprise several parcels). This implies an assessed value of $218/acre. Reviewing a small sample of parcels, it appears that the Assessor values most class 239 parcels at $2250/acre, and assesses them at 10% of that, or $225/acre.

One might compare this to the Illinois Society of Farm Managers and Rural Appraisers’ report, which includes but doesn’t break out Cook County, and indicates sales prices in Northeastern Illinois range from $5500 to $40,000 per acre.

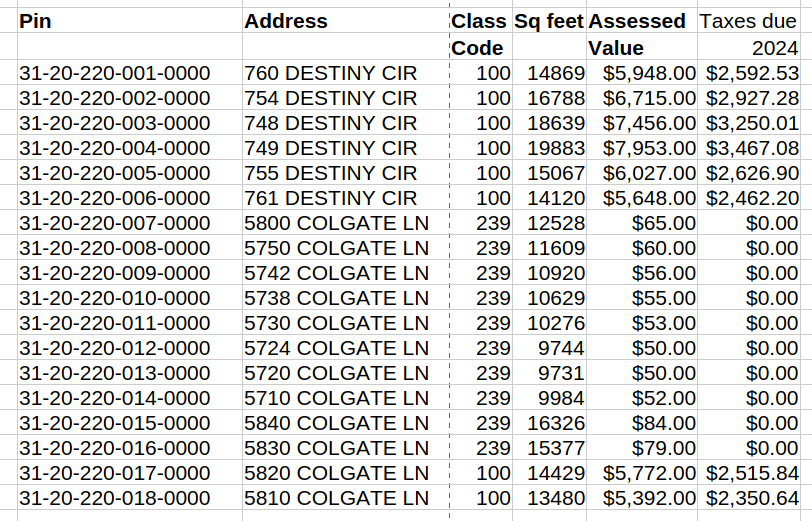

There’s no minimum parcel size for a “farm” under class 239. Thus, we have a series of 18 small vacant lots in Matteson: 31-20-218-001-0000 thru 31-20-218-018-0000. All of these appear to be empty lots, awaiting the construction of houses. Eight of them are classified as vacant land, with assessed values ranging from $5392 to $7953 (differences apparently due to differing sizes). Taxes due on these in 2024 range from $2351 to $3467 (excluding overdue taxes from the prior year, but including interest charged). But ten of these similar lots are class 239, farmland, assessed at $50 to $84. The County issues tax bills of zero for these parcels. This is claimed to be due to 35 ILCS 200/18-40, which states

If the equalized assessed value of any property is less than $150 for an

assessment year, the county clerk may declare the imposition and collection of

all tax for that year to be extended on the parcel to be unfeasible and

cancelled. No tax shall be extended or collected on the parcel for that year

and the parcel shall not be sold for delinquent taxes.

However, these parcels are assessed at $50 to $84. Applying the equalization factor of 3.0163 results in EAV greater than $150. In response to my inquiry, the Cook County Treasurer explained that, even tho equalized assessed valuation is printed on the tax bill, it isn’t used for taxation of farm properties. Here are the 18 parcels:

18 vacant lots in Matteson

I don’t know why 10 of these properties are assessed as farmland while 8 are not.

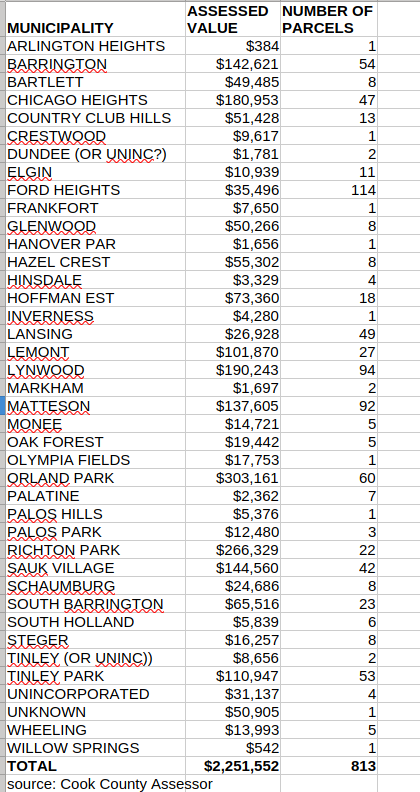

Countywide, the 813 class 239 parcels have a total assessed value of $2,251,552. While the Assessor’s records are imperfect (there being, for example, no “Dundee” municipality in Cook County), it appears that only 37 of the County’s municipalities (plus a few unincorporated areas) contain class 239 parcels. The tally is shown in the following table. Keep in mind that these are assessed value, 1/10th or less of the actual market value.

Summary of Class 239 parcels by place

While class 239 is a great bargain for owners of “farmland,” the inequity doesn’t seem, by itself, to have a major effect on the financial condition of the taxing bodies. For example, Ford Heights has the largest number of class 239 parcels, 114. Total class 239 assessed value in Ford Heights is $35,496. If this land was subject to equalization like other parcels, the equalized assessed value would be $107,067. As noted above, the Assessor seems to undervalue class 239 parcels, but even if we assume undervaluation of 75%, the total EAV of these parcels would be $428,268, for a net increase of at least $392,772. (I say “at least” because some or all of the class 239 parcels may be assessed at less than $150 and therefore completely untaxed.) The latest report I can find for Ford Heights total EAV, from 2022, is $14,201,062. Thus, if my assumptions are correct, and tax levies don’t change, then the typical property owner would save just 2.76%, Longer-term, landowners might be encouraged to develop their parcels, with housing or other improvements, so the benefit over time might be greater and might not only be financial. There would be no expense to the Village or other taxing bodies.

And of course the captioned illustration at the top of this post, 7+ acres in desirable Hanover Park, easy walk to Metra, adjacent to residential areas (or suitable for retail/commercial use), takes advantage of class 239 to pay taxes of less than $200/year.

The current locally assessed value of these 59,886 parcels totals $490.23 million. By ordinance, these assessments are 10% of what the Assessor estimates to be the market value of these parcels, implying that they’re worth $4.902 billion. Of course there’s also a “multiplier” of 3.0163, meaning the taxable value is $490 million X 3.0163 =$1.478 billion. Tax rates vary around the County, but in Chicago currently (before expected increases) is 7.02%. Meaning that owners of vacant land need to pay $1.54 billion X 7.02% = $103 million.

The County Board decided that vacant land, like residential real estate, should be assessed at 10% of estimated value. Commercial and industrial land is assessed at 25% of value (with exceptions for special favors). The Board could, by ordinance, apply this 25% factor to vacant land also. Which would raise something like $490 million X 1.5 X 3.0163 X.0702 = $155 million/year. Without taxing any housing; without taxing any business. Without taxing anybody who can’t afford to own land. Now $155 million may not seem like a lot, given that the City of Chicago is running something approaching a $1 billion annual deficit, Chicago Public Schools hundreds of millions more, and of course many suburban Cook County taxing bodies are in deficit. But $155 million is just the start.

If you are owner of a vacant lot, and you receive notice that your taxes have more than doubled, what will you do? You could sell the lot, but who would buy it? Probably somebody who wants to build housing, or a commercial business, or something else that serves the community. Or you might decide to build something yourself. Either way, this contributes to better housing supply or increased job opportunities.

Also, that $155 million/year is just for actual vacant lots, coded by the Assessor as class 100. There are also 25,180 parcels labeled as “vacant land under common ownership with adjacent residence” (class 241), also assessed at 10%. These are assessed at $123 million. By the same calculation as we used for vacant lots, assessing these like other nonresidential property could yield an additional $39 million, and some of the parcels would be used for new housing (including accessory dwelling units) or other useful projects.

This amount of revenue is not going to solve all the financial problems of Cook County local governments, but it would be a start, would cost practically nothing to implement, and would have the side benefit of increasing jobs and housing.

Many vacant lots are not taxable, because they belong to the City of Chicago or other government agencies. The above calculations omit such lots. DePaul’s Institute for Housing Studies has examined vacant land in Chicago, including City-owned parcels, and provides some analysis here.

This is not a complete remedy for Chicago’s and Cook County’s financial (and other) difficulties. But it should be an element in any plan to achieve prosperity and justice.

This new book by Strong Towns head Chuck Marohn (and Daniel Herriges) is worthwhile for anyone who wants to understand where America’s “housing crisis” came from. The history is important: How did we get here? He goes thru how housing was financed a hundred years ago, federal programs enacted in response to the 1929++ economic depression and subsequent disruptions, subsequent federal programs, and the dilemma we have today.

About 2/3 of American households are homeowners, they have (or hope to obtain) “equity” in their property, and they really don’t want to see the economic value of their holdings decline. Many of them are already stressed by the cost of paying their mortgages, taxes, maintenance expenses, and other costs of living. Not to mention the cost of owning and operating automobiles, as in most communities life without one is quite inconvenient.

The remaining third are renters (plus the unhoused). Many of them are also under economic pressure, as rents in recent decades have outpaced incomes. They might like to see housing prices decline, or more precisely to see the housing they want become easier for them to afford.

So there are big interests who want housing costs to decline, and who don’t want the price of housing to decline.

Part of the problem, as Marohn sees it, is that nowadays housing is built, financed, and often managed at a national scale. These folks are professionals who can deal with complex zoning and building code requirements. So part of the remedy is for local governments to make it easier for small-scale, local builders to make housing. This would include allowing an increase in density by right, such as backyard cottages, accessory apartments, or a two or three unit building in areas which have been restricted to single family.

This isn’t wrong, and I have enough personal experience dealing with building and zoning officials in a “progressive” community to know that improvements would be helpful. Even Brandon Johnson claims to be aware of the problem.

Working thru the book, I kept wondering what happened to the land value tax, which I know Marohn has supported. When I got to the example on “Financing Backyard Cottages” where he notes that one advantage would be additional property tax revenue, it sure looked like LVT has been tossed aside. Finally, toward the end of the penultimate chapter, he says “the land value tax… is perhaps the best mechanism to overcome neighborhood stagnation and decline.” Well it was nice he was able to fit this in.

I do recommend this book to anyone interested in realistic ways to get more housing built, or just in finding out how we got where we are. However, if you want to know how the whole problem could have been avoided by getting public revenue primarily from the value of land and other privileges, you’ll want to look elsewhere.

Tech billionaire wants to solve economic inequality, among other problems, by building a new city funded by land value tax. As described here, alternate source here.

Of course there are all kinds of issues involved in building a new, freestanding city, but it’s encouraging that he wants to start on a sound economic basis. Thanks to Bob Jene and Edward Miller for the tip.

Some land in Woodlawn (15 years ago). Image credit: Eric Allix Rogers CC BY-NC-ND 2.0

A D Quig reports in Crains that the City of Chicago’s Housing Commissioner says “everyone who lives in Woodlawn now should be able to stay in Woodlawn.” This can be a challenge as housing costs in the area rise. According to Crains (not corroborated by any press release I can find on web sites of the Department of Housing or the Mayor’s Office), support for housing affordabiity in the area will involve six strategies:

Right of refusal for large apartment building tenants if a landlord seeks to sell his or her building

Helping apartment building owners refinance properties to keep renters in place with affordable rates

Giving grants to long-term homeowners to help with home repairs

Financing the rehab of vacant buildings

Setting guidelines for how city-owned, vacant, residentially zoned land can be developed into affordable or mixed-income housing

Requiring developers that receive city-owned land to meet enhanced local hiring requirements

Details, of course, are yet to be defined, and the whole thing requires action by the City Council. Still, assuming that the program is effectively structured and implemented, what we have is the designation of a privileged class– people who live in Woodlawn– receiving benefits that might otherwise accrue to another privileged class — people who own land in Woodlawn, with a new layer of bureaucracy established (or repurposed) to administer it, including investigating and monitoring the reported income and behavior of the people who are granted permission to live in the area.

Whereas, under a land value tax, the area would now have little vacant land, presumably a lot more housing, probably quite “affordable.”

Of course if you’re the Mayor, you do what you figure is politically feasible and within your power, not what is morally right and economically efficient, but would require persuading a lot of uninformed voters and obtaining cooperation from quite a few other governmental actors.

Vintage 2012 view of Silicon Valley showing major employers. “Silicon Valley IT Company Topography” by Wayan Vota is licensed under CC BY-NC-SA 2.0

Or more precisely, who owns Santa Clara County? With the cooperation of local officials including the County Assessor, a consortium including the Mercury News has determined who owns the greatest value of real estate in the County. Tech giants Alphabet and Apple are second and third, but the number one owner turns out to be Stanford University.

Some other important information:

Proposition 13 is mentioned, but the incentive which keeps old people in their homes which become unaffordable to most families is not explored.

Local opposition to development, preventing housing construction which might otherwise occur, is discussed.

Stanford’s existing holdings include commercial property, but their current acquisitions seem mainly to provide housing for some of their elite employees. These people are able to buy houses at favorable prices (relative to the area), however Stanford retains the land and retains the right to buy the house back eventually. Local non-Stanford people complain, of course, but do not offer to sell their properties at a discount.

Apparently California practice is to assess all real estate, even that which is exempt. This enables meaningful estimates of ownership even tho $13.3 billion of Stanford’s $19.7 billion in real estate is exempt.

Several local officials were interviewed. They don’t discuss how it feels to know that your opposition, Apple and/or Google, has control of much of your communications and might be monitoring them.

Reportedly, taxes of 163,036 parcels in Cook County were not paid on time. This comprises 2018 taxes which should have been paid in 2019. and amounts to 8.7% of all parcels in the County. For a dozen south Cook County municipalities, this amounts to 20% or more of total parcels. Counts by municipality are posted separately for south, west, and north Cook. All sources show the percentage of parcels with unpaid taxes within the City of Chicago as 9.9%.

Separately, the reports show that only 7.8% of the delinquent taxes offered for auction in 2018 were bought by investors, which might imply that the remaining parcels are considered worth less than the taxes owed.

Unfortunately the source doesn’t tell us how many of the parcels are vacant, residential, commercial, or other uses, and gives no historical context, so we don’t really know how any of these figures compare to prior years. But regardless, the current numbers are alarming.

Suppose that the real estate tax system was changed, so that improvements would be tax-free while the value of land as vacant would be heavily taxed to make up the difference. For vacant parcels, construction of houses or other structures would not increase the tax. For parcels which contain improvements, taxes likely would be lower than now, and improvements would again be tax free. Just a thought.

Maybe expanding tax-exempt institutions raise land prices?

Crains tells us that a strikingly-designed two flat, less than 30 years old, is worthless. Well, they didn’t say it quite that way, but it was sold for $1.9 million to a buyer who will demolish it. So the $1.9 million was for the land. I don’t know whether any developer of housing or anything else taxable would have paid nearly that much for the site, but the buyer was tax-exempt Illinois Masonic Medical Center. Their exempt status of course made the land more valuable to them. Which raises the interesting question of whether buying land in the path of such an institution’s expansion might be a profitable strategy. Of course, a fair-minded community might decide to tax land used for hospitals at the same rate as land used for housing and other useful things. But we’re not there yet.

“Taxes – De Standaard” by Stijn Felix is licensed under CC BY-NC-ND 4.0

Great story by Hal Dardick in today’s Tribune explaining the real reason the Lincoln Yards TIF had to be Rahm’d thru the City Council before the new Mayor took office. The area just barely qualified as a TIF, and pending new assessments were going to rise enough that it would no longer be eligible. According to the story, it’s uncertain whether the new Mayor could have stopped the project, but she settled for what appear to be minor concessions.

Of course, the whole idea behind TIF’s is that money can be pulled from general revenue into giant slush funds, which the Mayor (and others) can manipulate with little oversight. Meanwhile, there’s little left for routine maintenance, replacement of infrastructure and funding of government schools and other services. Which increases the “need” for TIF’s.

Dardick’s article goes into considerable detail, includes a link to a recent report by Lincoln Institute (no relation to Lincoln Yards, afaik). He does say “land” when I think he means “land + improvements.”

One counterfactual that Dardick doesn’t bother with: What would have happened if Joe Berrios was still Assessor? Would he have nudged down some values to keep the area eligible? Or, to look at it the other way, suppose the current Assessor, who appears to be more conscientious, had been in office since 2013. Perhaps the earlier figures would have been higher, so the increase would be less?

We’ll never know, and it shouldn’t matter. In a well-run city, TIF’s wouldn’t be needed, and a well-informed electorate wouldn’t tolerate them.

Christopher Flavelle’s recent Business Week article looks at how rising sea levels can affect ownership of newly-submerged land. Part of the problem, of course, is that owners of these parcels want the government (Corps of Engineers, local authorities, somebody!) to use expensive artificial means to preserve or recover their properties, but of course don’t particularly want to pay for the service. Complicating the situation is the public trust doctrine, as applied in the various coastal states, which prohibits private ownership of submerged land. So if the land is recovered, who owns it?

A land value tax won’t prevent land from being submerged, and won’t clarify ownership, but it will importantly change the incentives. The article cites one case where the landowner continues to pay real estate tax [presumably a modest amount, but the article does not say] on the submerged parcel. ‘“It’s Gulf-front property,” says Levenson, who now lives in Tennessee. “Someday it will be valuable.”’

Suppose, instead, that the rental value of land was the sole source of public revenue. The land might someday be very useful, and might have a large rental value, but could never be sold for a high price. End of controversy. The water rises, the owner avoids the taxes by relinquishing the land. Unless the rest of us are obligated to pay to enrich a few coastal owners, this is the just and efficient way to proceed.